- Bank of England to hike rates again Thursday

- But will gift GBP a one-way ticket lower say analysts

- GBP sentiment is already poor

- Potentially allowing for a relief rally

- Especially if Bank says economic outlook has improved

- Since energy cap announcements

Image © Adobe Images

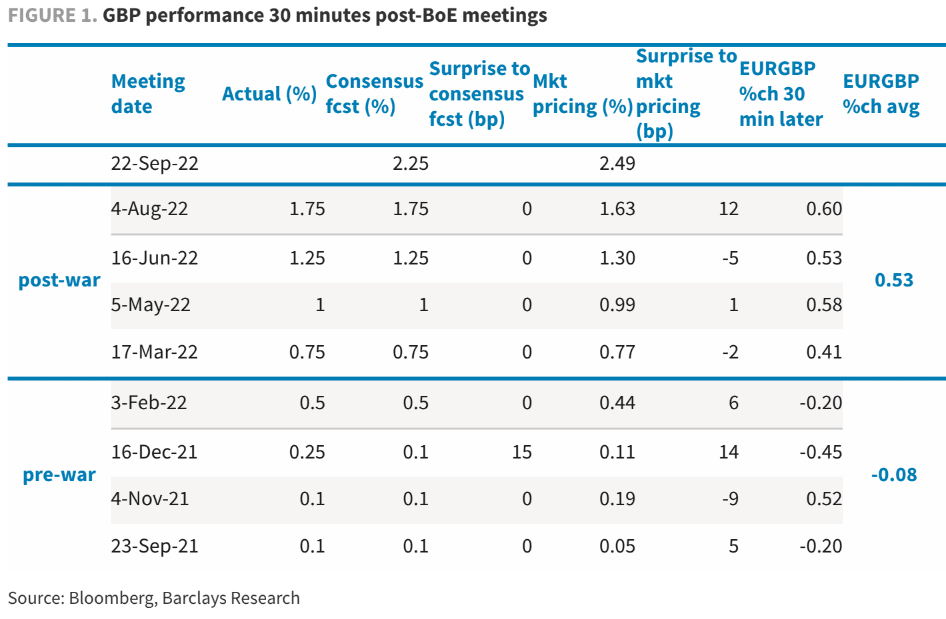

"Since the start of the Russia-Ukraine war, GBP has weakened after every BoE meeting, against the UK's stagflation backdrop," says Themistoklis Fiotakis, Head of FX Research at Barclays.

The observation is a sobering reminder for long-suffering holders of the UK currency who have seen their international purchasing power slide through the course of 2022, as it comes just hours before the Bank's September policy decision.

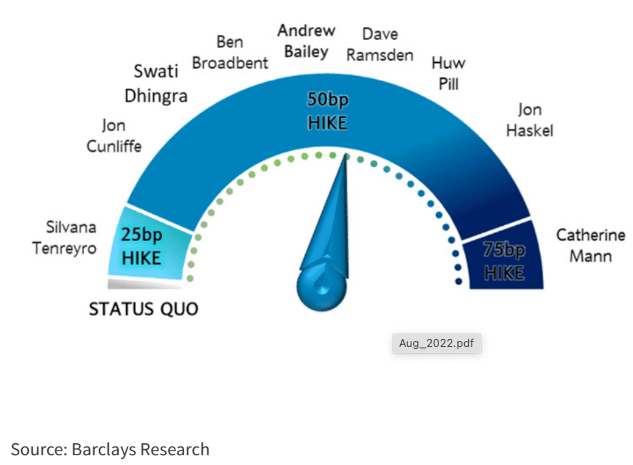

Money markets show investors are pricing a 75 basis point hike as they demand more forceful action by the Bank on UK inflation; they are priced for a further 125 basis points over the two remaining meetings of 2022.

But disappointment is likely, according to Fiotakis, "we expect the BoE to hike 50bp at the upcoming 22 September meeting, with a clear dovish tilt".

Such an outcome would be the now-familiar response of a central bank long accused by economists of being 'behind the curve' on inflation.

Pound exchange rates would likely respond by falling and extending their steady decline.

"An under-delivery to market pricing, or a dovish tilt already at this meeting – for instance, a split vote by the MPC – would see rate expectations lowered and GBP underperform," he adds.

Above: The Monetary Policy Committee holds an inherently 'dovish' bias.

The Pound to Euro exchange rate has fallen 3.75% in 2022, with 1.1435 seen at the time of writing, meaning bank account transfers are done at approximately 1.12 according to our data, meanwhile specialist payment providers are seen offering rates around 1.14.

But Barclays says the British Pound would rise if the Bank hiked by an increment above what markets are expecting, implying a 100bp move would have the shock factor to send Sterling higher.

To shore up the Pound, Barclays says a sizeable hike would be needed to make UK monetary assets more attractive to international investors.

Like other similar countries, the UK faces a terms of trade shock in the post-Ukraine war period as its import costs surge amongst rising energy prices.

Given the government of Liz Truss has opted to spend more to mitigate the impact, Barclays says what happens to the Pound is largely in the remit of the Bank of England.

As the UK's monetary authority, the Bank can:

1) tighten policy more to raise savings, reduce external funding needs and anchor prices; or

2) tighten less to protect demand and allow FX depreciation to boost savings and moderate external funding needs.

"How the shock is split between demand damage and exchange rate weakness is a policy choice," says Fiotakis.

A below-consensus 50bp hike therefore looks to be an outcome that would spell certain decline for the Pound.

Heading into Thursday's update sentiment towards Sterling is near rock bottom, as such the prospect of a post-decision rebound cannot be ruled out.

This would likely be the case were the Bank to hike 75bp, thereby meeting market expectations, and inviting a classic 'buy the fact' knee-jerk response.

It is also possible the market takes some cheer from any suggestions by the Bank the UK economic outlook as improved since the government announced energy price caps for both households and businesses.

After all, it's been the Bank's recent forecasts that have been more of a weight on Sterling than the actual interest rate decisions.

"As soon as the BoE’s forecasts hit the wire, surprising markets by the Bank’s grim outlook for higher inflation and lower growth in the UK, GBP would start to sell off," says Fiotakis.

The Bank could also acknowledge the peak in inflation would likely be lower than they thought at the time of August's Monetary Policy Report.

Economists have slashed their forecasts for the peak in UK inflation as the government's energy price caps will lower the contribution of energy price rises.

In August the Bank had forecast a peak of 13% in inflation for October, but they will have to signal a revision lower.

They also forecasted a multi-month recession starting at year-end, but with inflation set to come in lower a mechanical uplift to growth is expected.

Such outcomes could push back against uncompromising investor pessimism and spark a relief-style short-term rally.