Financial markets are waking up to the realisation that no Greek government will be able to maintain their current committment to the debt programmes imposed by international lenders under existing frameworks.

With key European creditors looking increasingly intransient in the face of domestic elections there is a realisation that a radical outcome to the long-running crisis is likely.

And this, according to one financial analyst, makes Greece the financial risk flash-point of 2017.

“The odds of another Greek crisis are rising. The long-lasting stand-off between the IMF, Germany and Greece has heated up, and no easy solutions are in store. The current approach will inevitably lead to another escalation, maybe also Grexit,” says Jan von Gerich, Global Fixed Income Strategist at Nordea Markets in a note to clients.

By Grexit we would assume von Gerich refers to Greece leaving the Eurozone, as opposed to the European Union.

The implications of such a move for the Euro are hard to gauge - 1) Does Greece exiting bring into question the Eurozone, in which case it could be negative or 2) Does Greece exiting strengthen the remaining members in which case the Euro rises rapidly to fairer valuations?

Whatever the case, the lead up to any resolution will be laden with uncertainty and if there is one thing currencies don’t like, it’s uncertainty.

The prospect of Greece exiting the Eurozone were made all the more palatable today when Wolfgang Schäuble, Germany’s finance minister, says Greece must leave the Eurozone if it wants some of its debt cut by Germany and fellow European creditors.

He told German broadcaster ARD that debt forgiveness would be in violation of European rules:

“We can’t undertake a debt haircut for a member of the European single currency, it’s ruled out by the Lisbon Treaty. For that, Greece would have to exit the currency area.

“The pressure on Greece to undertake reforms must be maintained so that it becomes competitive, otherwise they can’t remain.”

Schäuble has repeatedly raised the prospect of Grexit, going as far as linking more significant debt relief to Grexit.

He maintains that writing down the principal value of Greek loans would be legally possible only if Greece left the Euro area.

Market Concerns Increasing

Even if a Greek exit from the Eurozone were a good thing for the Euro, currency markets would first have to contend with the uncertainty to be found in the lead up to the exit.

Greek bond yields have risen again lately as investors demand more coupon payments for holding Greek debt which is now deemed to be more risky.

“Further, the inversion of the yield curve has intensified, signalling mounting worries of a looming crisis. While the levels are far from those seen in early 2016 or 2015, concerns have clearly risen,” says von Gerich.

The analyst notes Greece alone would probably not be enough to trigger another broader debt crisis in the Eurozone.

“However, coming at the same time as political risks in especially France are causing tremors, the Greek worries have more potential to intensify the market impact. As a result, the Greek developments clearly warrant a cautious stance on EUR government bond markets for now,” says von Gerich.

With German elections later in the year the current administration cannot afford to appear soft on Greece or risk being booted out.

The same could arguably be said for administrations in France and Holland where elections are nigh. Therefore Greece might find few friends in the rest of Europe ensuring they are nudged towards the Grexit door.

This should keep demand for the Euro capped.

"Financial markets are focused on the French presidential election, but there is another, nearer-term catalyst for euro weakness: the stalled talks between Greece and its international creditors. If the impasse isn't resolved by the time Eurozone finance ministers meet on Feb. 20, politics will make it hard to resolve afterwards. And if the IMF pulls out, both Germany and the Netherlands have said they won't participate further," says Mathieu Reaud at UBS.

Reaud, an options trader at UBS, is looking for the EUR/USD to fall as a result.

Financial Crisis Brewing

The financial analysis from Nordea comes as popular unrest to the IMF reform programme starts to increase.

Farmers are stepping up protests over unpopular creditor-mandated austerity measures including higher taxes.

The Guardian’s Helena Smith reports:

“In a move that will put the Greek government under further pressure to bow to their demands, farmers and stockbreeders escalated their protests today blockading the customs post at Kristallopygi on the country’s border with Albania.

“Describing the move as symbolic, Dimitris Moskos who sits on the committee representing farmers in the region, said the blockade would last 24 hours.”

It follows protests in Athens on Wednesday by Greek firefighters, who say a third of jobs are at risk because of hiring restrictions placed on the public sector by the terms of Greece’s international bailout.

Germany Wants Austerity

While Germany’s finance minister is happy to show Greece the Eurozone’s exit door, another German Klaus Regling believes Athens will find a path forward, but at a cost.

Regling is the managing director of bailout fund the European Stability Mechanism and argues:

“A sober look at the facts shows that Greece’s debt situation does not have to be cause for alarm. The European Financial Stability Facility and the European Stability Mechanism, the eurozone’s rescue funds, have disbursed €174bn to Greece. We would not have lent this amount if we did not think we would get our money back.

“The solution for Greece lies not in additional debt relief, but in the government implementing reforms so as to avoid delays in the issuing of the next tranche of the ESM loan.

“Investors understand the ESM framework and recognise the commitments of Greece’s European partners.

“Past experience shows that making loans in exchange for reforms works. It is no coincidence that Ireland and Spain today have some of the highest growth rates in Europe and very low funding costs after successfully completing rescue loan programmes with demanding reforms.”

Therefore, Regling wants Greece to stick with its austerity agenda confirming an uncompromising Germanic approach to the issue.

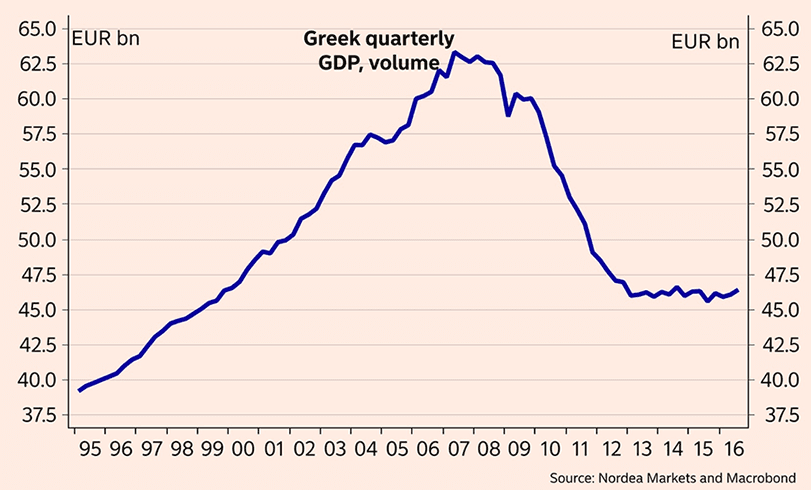

This is at odds with an under-pressure Greek population who have seen their economy rise with the Euro, only to fall back to levels last seen in the 20th century.

Regling’s view is also at odds with bail-out partners the IMF who believe austerity might not be the way forward.

“The IMF and Germany fundamentally disagree on how the debt crisis should be handled. The IMF has admitted it made mistakes in the first Greek programme, and now would want to rely less on austerity and more on structural reforms and growth-friendly policies. Germany, in turn, continues to push for hard austerity as the only viable solution,” says von Gerich.

The Nordea analyst believes the IMF’s involvement matters, not only because of its expertise, but also because both Germany and the European Stability Mechanism have said the programme can only continue with full IMF participation.

The IMF, in turn, has become even less willing and able after its debt sustainability analysis reportedly showed Greek debt ballooning to 275% of GDP by 2060.

“Buying time with temporary compromises will not work anymore. The IMF needs to make a decision on its participation, and the European creditors need to live with the consequences,” says von Gerich.

Markets are waking up to the fact that the current approach to the Greek problem will not lead Greece out of its problems.

“It looks equally clear that none of the main players are going to change their mind quickly. After all, the much-vaunted economic recovery in Greece is in fact not any noticeable recovery at all,” says von Gerich.

A change of government in Germany or Greece might change things, but in the current setup, von Gerich argues the programme is doomed to fail, “leaving the door for Grexit wide open”.