The recent fall in the British pound exchange rate complex is expected to push inflation rates higher argue analysts as they release their initial forecast changes following the UK's vote to leave the European Union.

The UK imports more than it exports therefore it relies on a strong exchange rate to ensure the cost of those goods remain low at their point of purchase by the consumer.

It therefore goes that any depreciation in the UK’s exchange rate could put upward pressure on prices.

Sterling has fallen notably since the EU referendum results were announced and unless there is a recovery to pre-Brexit exchange rate levels soon, inflation will likely respond by moving higher.

“We estimate a 10% depreciation in the nominal effective exchange rate (on a trade weighted basis) would add between 1.0 and 1.5 pp through the forecast horizon, taking headline CPI to an average of 1.0% in 2016 and to 2.5% in 2017,” says Fabio Fois at Barclays.

Considering that the GBP/USD exchange rate was 8% lower at one stage on Friday the 24th, we would imagine a 10% decline in GBP TWI is achievable.

Consistent with expectations that the pass-through will impact NEIGs and energy related-services prices, Barclays forecast core inflation to average 1.7% this year and 2.3% next year.

Regarding the trajectory, Barclays forecast headline CPI to rise well above the Bank of England’s mandated target of 2%.

Inflation should peak in Q2 17, before gradually declining and stabilising around the target level in Q4 17.

Upside risks to these projections exist in the form of the outlook for food prices, however.

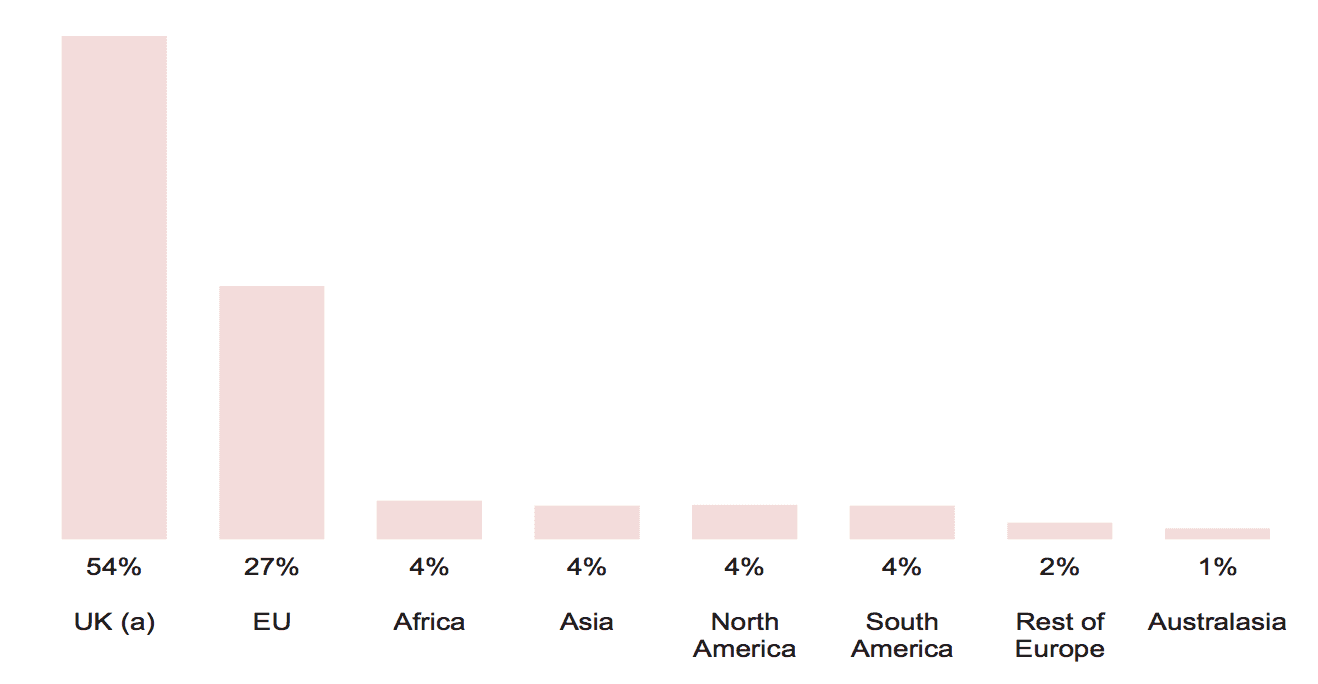

Currently the UK produces 54% of its own food while importing 27% from the EU.

Source: Department for Environment, Food & Rural Affairs

In the case of an exit, agricultural imports would become more expensive should no Free Trade Agreement be reached.

“Given supermarket price competitiveness, food prices would likely rise quickly in response to increased costs,” says Fois. “However, given that typical supermarket-producer price contracts are fixed for between one and two years, this risk appears more muted in the short term, although it could be an important consideration from mid-2017 and beyond.”

The European Common Agricultural Policy (CAP) has historically faced criticism for artificially pushing up food prices.

On an EU exit, the UK is unlikely to remain a part of the CAP.

“However, we do not believe exiting from the CAP would significantly impact food prices,” says Fois, “the CAP no longer pushes up food prices as it once did due to major reforms implemented during the past decade.”

Barclays note the nominal assistance and protection coefficient ratios for the EU are now not too dissimilar from the OECD average, resulting in European food prices not being significantly higher relative to world food prices.

We can also report that investment bank JP Morgan have also raised their inflation forecasts for the United Kingdom.

Analysts say they see inflation in the fourth quarter of 2016 rising to 1.1% and surging to 2.2% in the second quarter of 2017.

This is a notable surge and typically we would expect the Bank of England to react by raising interest rate to fulfil their mandate of keeping inflation at the 2% level.

However... this time the Bank is likely to let inflation breach the top side.

No Bank of England Interest Rate Rise in Response to Inflation

Typically, the Bank of England would act against rising inflation by raising interest rates.

Higher interest rates tend to decrease the quantity of money coursing through the economy as spending is cut back, thereby lowering inflation.

However, such a move could exacerbate any slowdown in UK growth owing to Brexit-inspired uncertainty.

“Despite the weakening of the GBP, we expect the BoE to lean against elevated uncertainty and financial market volatility by further easing monetary policy. Specifically, we would expect the BoE to cut the bank rate by 50bp; this would bring the policy rate by end-2016 to zero,” say Barclays.

The BoE could also decide to deploy QE again by announcing a new asset purchase programme of approximately £100bn-£150bn.

There would be a clear policy objective to maintain lending channels.

Therefore, Barclays believe other relevant and likely policy levers would include a targeted Funding for Lending Scheme (TFSL) towards export firms for the interim period of trade-deal negotiations.

This could be combined with zero capital weights against loans to these firms.

This very accommodative monetary policy response would likely to be sustained until

uncertainty was resolved and macroeconomic activity stabilises.

“The GBP depreciation and the pass-through into prices would allow the BoE to remove gradually some of the policy accommodation as the economy stabilises and there is more clarity over time about the trade and regulatory framework,” say Barclays.

So the outlook for interest rates has been turned on its head - lower for longer is likely to be the theme going forward.

And lower for longer spells a weaker pound for a longer period of time.