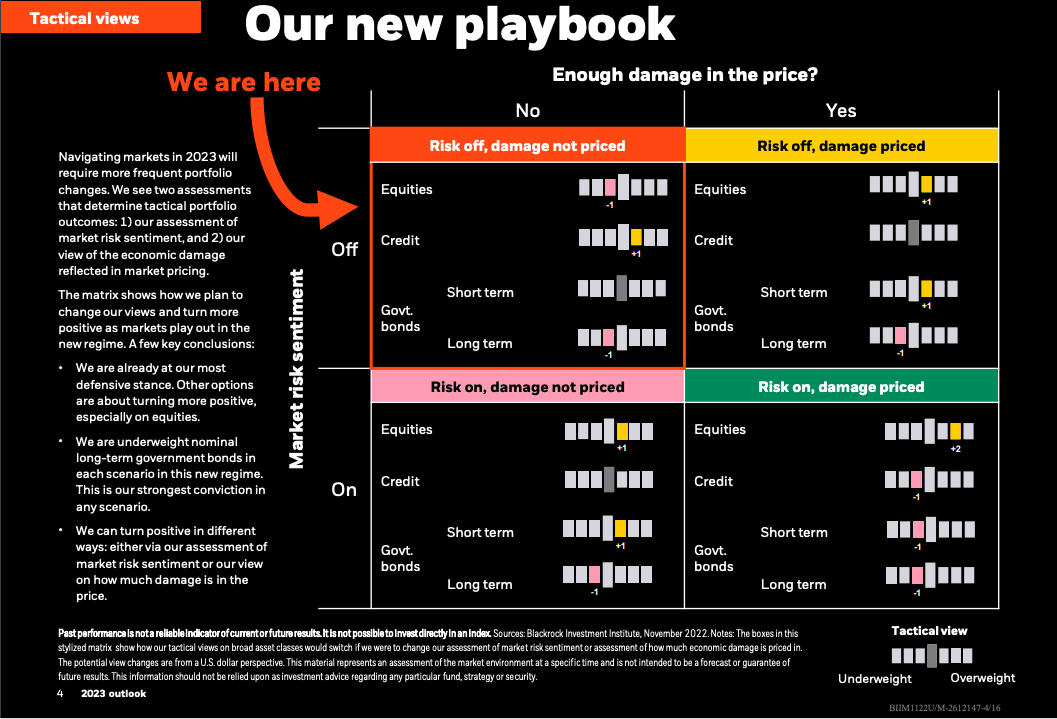

- Time to buy stocks will arrive in 2023

- As central banks recoil at economic slowdown

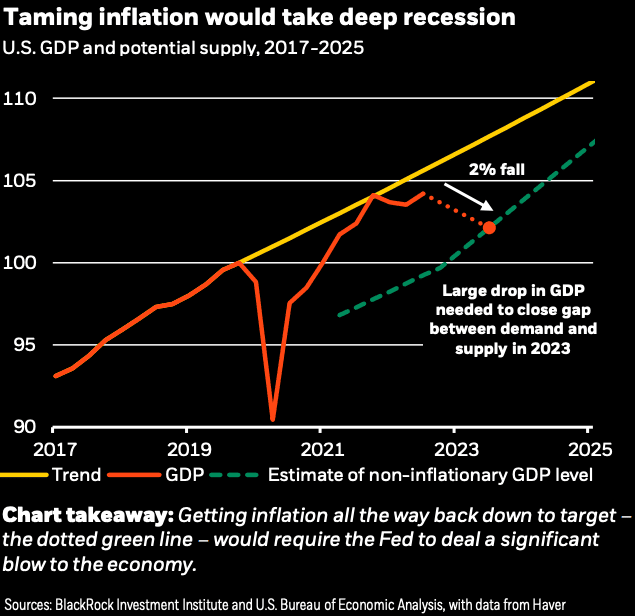

- But they will fail to bring inflation back to 2%

- "Equity valuations don't yet reflect the damage ahead"

- "A new investment playbook is needed"

Image © Adobe Stock

Blackrock says a deep recession must be engineered by developed market central banks if inflation is to fall back to the 2.0% target, but they will stop hiking as soon as "the damage becomes real".

As a result, inflation will remain persistently higher than has been the case over the past two decades.

"A recession is foretold; central banks are on course to overtighten policy as they seek to tame inflation," says Philipp Hildebrand, Vice Chairman at BlackRock.

Blackrock is the world's largest asset manager and where they go has significant implications for market price action and sentiment.

"We expect to turn more positive on risk assets at some point in 2023 – but we are not there yet," says Hildebrand.

In a year-ahead research note, Blackrock paints a picture of a decidedly more difficult investment environment to navigate and as a result, they don't see the sustained bull markets of the past.

"A new investment playbook is needed," says Hildebrand. "Central bankers won’t ride to the rescue when growth slows in this new regime, contrary to what investors have come to expect."

This is because they are actively seeking to cool demand in the economy to bring inflation down.

But central banks will eventually back off from rate hikes in 2023 as the economic damage they are partly responsible for becomes reality.

As such, Blackrock expects inflation to cool but stay persistently higher than central bank targets of 2%

And, "equity valuations don't yet reflect the damage ahead."

The asset manager says it will turn positive on equities once they assess the damage is priced.

Blackrock acknowledges the new 'regime' is shaped by supply-side shortages, a familiar theme by now in a world of high energy and commodity prices and for developed market economies this shortage includes workers.

"Central bank policy rates are not the tool to resolve production constraints; they can only influence demand in their economies. That leaves them with a brutal trade-off," explains Hildebrand.

He says they either get inflation back to 2% targets by crushing demand down to what the economy can comfortably produce now (dotted green line in the chart), or live with more inflation. For now, they’re all in on the first option.

"So recession is foretold. Signs of a slowdown are emerging. But as the damage becomes real, we believe they’ll stop their hikes even though inflation won’t be on track to get all the way down to 2%," says Hildebrand.

Blackrock expects some production constraints could ease as spending normalizes but three long-term trends are set to ensure production capacity is constrained.

1) An ageing population means continued worker shortages in many major economies.

2) Persistent geopolitical tensions are rewiring globalization and supply chains.

3) The transition to net-zero carbon emissions is causing energy supply and demand mismatches.

"Our bottom line: What worked in the past won’t work now," says Hildebrand.