Image © Adobe Images

The rise in UK sovereign bond yields "has only just started", according to new research released by Berenberg Bank.

Analysis from Berenberg shows there are four reasons to expect a rise in the yield paid on government bonds with a ten-year maturity over coming months and years:

1) Slowing BoE purchases

2) Net issuance remains high

3) Confidence is improving

4) Inflation expectations are rising

"Further upside surprises for key economic data such as GDP and underlying prices should raise benchmark yields in coming months," says Kallum Pickering, Senior Economist at Berenberg Bank in London.

The immediate implication from a currency angle of such a forecast is that this should be supportive of the Pound.

The Pound tends to benefit when UK yields are rising as this attracts inflows of foreign capital from investors looking for higher returns.

The major caveat here is that UK yields should be rising faster than yields in other countries as this is a relative dynamic.

This relative outperformance on UK yields can be achieved if the Bank of England reduces the amount of government bonds it purchases faster than other central banks plan to do so.

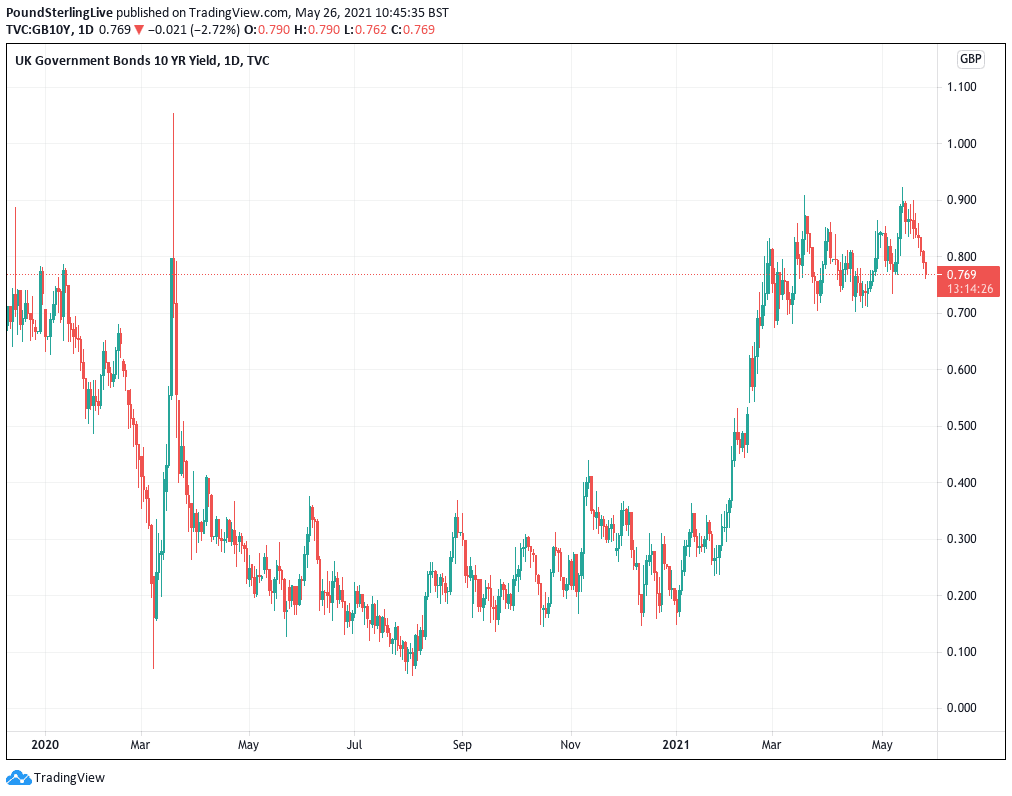

The call for higher yields on gilts - the name for UK sovereign bonds - comes as yields continue to lift from the record lows triggered by the aggressive purchase of government bonds by the Bank of England via its quantitative easing programme.

The dynamic is such: the greater the demand for a bond, the lower the compensation paid by the issuer those buying that bond (this is the yield).

But lower demand for the bond would translate into greater yields as the issuer must pay greater compensation to attract demand.

Berenberg note that the Bank of England has accounted for around 92% of demand for freshly minted gilts from February 2020 to April 2021 as the government ramped up issuance to finance its response to the Covid-19 pandemic.

During this time yields plummeted.

But remove that demand from the Bank of England and gilt yields inevitably rise, particularly if the government continues to issue substantial amounts of debt.

The Bank of England said on May 06 they were on course to end the current programme of quantitative easing by year-end, in line with expectations that the economy would recover from the Covid-19 crisis.

At the meeting they said they would 'taper' the amount of bonds they would purchase on a weekly basis to £3.4BN from £4.44BN to ensure the current quantitative easing envelope of £150BN stretches to year-end.

But the exit from the market of the Bank of England would come amidst ongoing issuance of new debt by the government to pay for the aftermath of the Covid-19 crisis.

"All else equal, the laws of demand and supply dictate that gilt yields will rise in coming months once the rate of new debt creation exceeds the rate at which the BoE purchases such paper. This may become a major contributor to rising yields once BoE net-purchases end," says Pickering.

The scale of UK government borrowing was again laid bare on May 25 when the ONS released their latest suite of Public Sector Net Borrowing statistics covering April 2021.

The deficit came in at £31.7BN said the ONS, an increase on the £28BN borrowed in March but below economist estimates for a reading of £32BN.

Even if borrowing forecasts are reduced somewhat going forward significant amounts of gilts must be issued to plug the shortfall between revenue and spending with the OBR predicting the government will need to borrow £233.9BN in 2021-22.

Another key influence on investor demand for gilts is inflation expectations: when investors believe inflation over coming years will rise they will demand greater compensation for holding government debt. After all, why hold bonds if it will just be eaten away by inflation?

Inflation expectations in the UK have rocketed during 2021, as they have the world over.

Berenberg notes that Retail Price Index-based five-year breakeven rates have risen from a low of 2.4% in April 2020 to a post-Lehman high of nearly 3.5% and are rising on trend.

The current breakeven rate of 3.5% equates to a c2.7% inflation rate based on the Consumer Price Index (CPI) – well above the BoE’s 2% target.

UK CPI rose 0.6% month-on-month in April, which is in line with the market's expectation but is a doubling of the March print at 0.3%.

CPI inflation for April rose 1.5% on a year-on-year basis says the ONS, a tick above the 1.4% the market was expecting and more than doubling the 0.7% print recorded in March.

{wbamp-hide start}{wbamp-hide end}{wbamp-show start}{wbamp-show end}

Demand for gilts is expected by Berenberg to decline as investors become more confident and opt for 'risker' and high-returning alternatives.

"Household, business and market sentiment has surged since the start of the year," says Pickering. "Over time, strong confidence should reduce precautionary demand for safe assets such as gilts and increase the rates at which the UK government can borrow."

Berenberg's researchers find it "somewhat surprising that bond yields have not yet risen further" given the above expectations.

"It may indicate that the market consensus, much like major central banks, does not expect the current period of strong growth and rising inflation to last beyond the recovery phase of the business cycle. Of course, only time will tell. However, we think there is good reason to believe that the ongoing strong cyclical upturn in the UK," says Pickering.

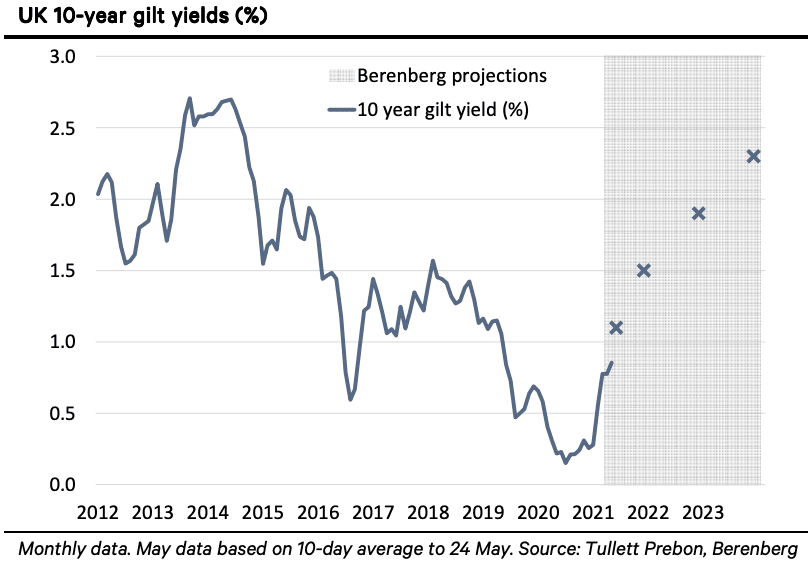

Berenberg forecast 10-year gilt yields at 1.5% by end-2021.

"Thereafter, further rises are likely during 2022 as the BoE reacts to upside inflation risks by outlining its exit strategy in early 2022 before hiking rates for the first in August 2022," says Pickering.