Image © Adobe Stock

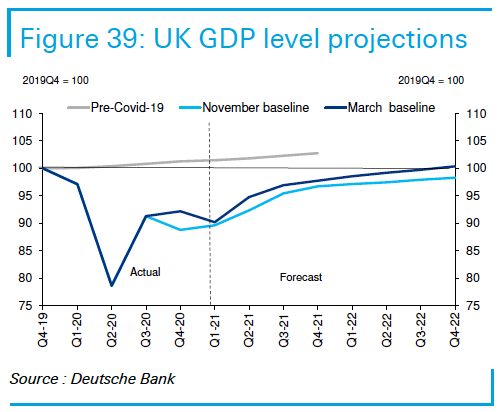

Economists at Deutsche Bank have raised their UK growth forecasts for 2021 and say the economy will be at 98% of its pre-pandemic size by year-end, allowing the Bank of England to begin the process of unwinding emergency support.

The upgrade to the UK GDP forecast profile contrasts to a downgrade for the Eurozone and maintain a strong forecast profile for the United States.

Deutsche Bank economists now see 2021 GDP growing by 5.7% (previous: 4.5%) and 2022 GDP rising by nearly 5% (previous: 5.2%).

"This should leave the UK economy at around 98% of its pre-pandemic levels of GDP by the end of this year. We expect the Bank of England to remain on the sidelines for at least the next two years," says Sanjay Raja, UK Economist at Deutsche Bank.

A supportive budget announced by Chancellor Rishi Sunak in early March and continued job and business support from the government are seen as being two positive developments that have allowed Deutsche Bank to upgrade their GDP forecasts.

We reported last week that Raja had told clients the UK economy will be boosted by a sizeable jump in consumer spending in 2021 as pent-up savings are unwound.

Over £160BN in excess savings has been accumulated by UK households during the pandemic, the initial burst in spending

over the second and third quarter will therefore likely be sizeable. It is assumed by Raja that roughly 7.5% of excess savings will be spent in the coming quarters.

"The UK’s excellent vaccination program should see restrictions phased out gradually over the first half of the year, resulting in a very strong Q2 and robust Q3," says Raja.

The Bank of England is meanwhile expected to remain on the sidelines for at least the next two years and keep interest rates unchanged.

However the window for negative rates now looks to be closing and Deutshche Bank say they now expect the BoE to turn its attention towards a plan for policy normalisation.

"To be sure, any policy tightening will likely be very gradual especially given the scale of fiscal consolidation pencilled in from 2023 onwards (roughly 1.5% of GDP). And with our view that inflation will fall back below the Bank’s 2% target from mid next year onwards, this should give the MPC ample flexibility to remain on hold before shifting to a tighter policy stance," says Raja.

Research from Barclays meanwhile suggests the UK economy had started awaking from its lockdown-induced slumber before the easing of lockdown restrictions on March 08.

"Even before restrictions have been lifted, activity indicators suggest a broad-based awakening of the economy," says Fabrice Montagné, an economist at Barclays.

Signs of life include: use of credit/debit cards, mobility and traffic, lending for mortgage and consumption, early travel booking and online searches.

Barclays expect GDP to already increase in March (by 1% m/m).

Noting that the pandemic in the Eurozone is not over yet and that restrictions have been extended, Deutsche Bank have meanwhile revised down their 2021 GDP forecast from 5.6% to 4.6%.

Economists are however optimistic on the outlook for the Eurozone's economy saying a strong rebound will transpire in the second half of the year, noting that although the region's vaccination programme has gotten off to a slow start it should nevertheless achieve its aims.

They expect Eurozone countries to start unwinding restrictions in the second quarter of 2021.

That said, Deutsche Bank's latest global forecasts were compiled ahead of news this week that the major EU countries had banned the AstraZeneca vaccine, which will likely significantly slow the vaccination programme.

The U.S. economy is meanwhile not subject to the same concerns as the Eurozone on the vaccination front and is forecast to grow 7.5% in 2021 on a quarter-on-quarter basis and 6.6% year-on-year.

"Even these robust figures understate the growth recovery we anticipate in the coming quarters," says Mathew Luzzetti, Chief U.S. Economist at Deutsche Bank.