Image © HM Treasury, Gov.uk

Economists warn the UK Treasury could risk derailing any post-covid economic recovery by raising taxes and slashing spending in a quest to rebalance the country's books.

Speculation has risen over recent weeks - courtesy of leaked plans emanating from the Treasury - that the Chancellor will start to tighten fiscal policy as soon as March.

The need to bring some balance back to the public finances is hard to dispute, but the debate of when and how this goal is achieved is growing and history has shown that rushing to consolidate finances too early can make the job of closing the gap between spending and earnings all the more difficult.

Jay Bryson, Chief Economist at Wells Fargo Securities says in the years following the financial crisis of 2008 many governments rushed to raise taxes and cut spending in order to shore up public finances, but the decisions in fact killed economic recoveries.

Back then, "many governments put in place significant fiscal stimulus to cushion their economies as much as possible from the contractionary effects of the global financial crisis. But as the downturn of 2008-2009 turned into recovery starting in 2010, concerns about debt started to mount and many governments then undertook fiscal consolidation," says Bryson.

"With the household sector still struggling to get back on its feet in the early years of the past decade, this fiscal tightening imparted a significant drag on many major economies," he adds.

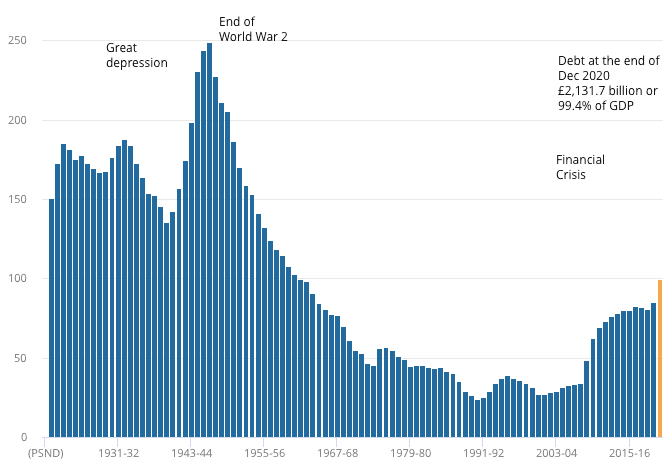

Above: Debt expressed as a percentage of GDP has reached levels last seen in the early 1960s. Public sector net debt excluding public sector banks, UK, financial year ending March 1921 to December 2020. Source: ONS.

The Conservative-Libderal Democrat coalition that took the reins of power in 2010 implemented a programme of austerity in order to try and bring the country's gaping structural deficit under control, efforts which ultimately succeeded.

But similar efforts in the Eurozone shows how economic growth can be killed off at a time when it is most needed.

"The Eurozone subsequently slipped back into recession starting in late 2011, and fiscal tightening exerted significant headwinds on economic growth in many other major economies in 2011 and 2012," says Bryson.

Bryson says it appears that another episode of fiscal tightening may be in store over the next two years.

The warnings come as the ONS reports the UK suffered its largest collapse in economic activity in history in 2020 meaning the country's economy must put in substantial GDP prints if the lost output is to be recovered and living standards return to pre-crisis levels.

Most economists now expect the UK to experience a strong recovery in 2021 as households spend pent-up savings and the economy is gradually unlocked.

But the scope of that recovery could have as much to do as decisions taken by Chancellor Rishi Sunak as it does with household behaviour.

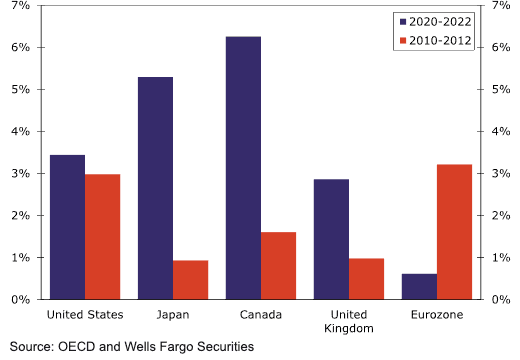

"Fiscal consolidation likely will occur in most major economies over the next two years, although to differing degrees. In some countries, specifically, Japan, Canada and the United Kingdom, the fiscal tightening that is planned in 2021 and 2022 significantly exceeds the degree of consolidation that was implemented a decade ago," says Bryson.

The following graphic shows the scale of tightening being envisaged by major economies now, compared to the previous crisis of 2010:

Above: Change in Cyclically Adjusted Primary Balance as percent of GDP. Wells Fargo says in some countries, the fiscal tightening that is planned in 2021 and 2022 significantly exceeds the degree of consolidation that was implemented a decade ago.

As can be seen, the scale of the fiscal retrenchment in the UK is likely to be far greater than was the case previously.

"Are these economies at risk of renewed downturns in the next year or so due to excessive fiscal consolidation?" asks Bryson.

Sunak has already imposed a pay freeze on at least 1.3 million public sector workers as part of efforts to contain government spending.

It was meanwhile reported in January that Sunak was considering raising corporation taxes as soon as March by as much as 19% to 23%.

Other tax hikes have been rumoured via leaks to the press, suggesting the Treasury is cautiously testing the waters.

Sunak commissioned a report in 2020 which suggested a £14BN tax raid could help the country's finances recover. In its report for the Treasury, the Office of Tax Simplification suggested that the Chancellor bring Capital Gains Tax into line with income tax.

This would mean higher rate taxpayers facing a flat rate of 40% or 45%.

Economists at the independent research house Capital Economics say they are confident that the UK economy will put in a strong rebound in 2021 as the UK covid crisis fades and lockdowns are eased, and finally removed altogether.

But Paul Dales, Chief UK Economist at Capital Economics, says he is wary that the Chancellor rushes to raise taxes.

"A major tightening in fiscal policy over the next couple of years is unnecessary and could prevent GDP from returning to its pre-crisis trend," says Dales.

In addition, by raising taxes the UK could be sending a negative message to foreign investors, just as the country fights to establish itself as a business friendly destination in the wake of Brexit.

"The government is rightly looking for ways to address the public deb," says Alpa Bhakta, CEO of Butterfield Mortgages Limited, which has asked 885 investors what they think of rumoured tax hikes. "BML’s research shows the tax could in fact drive investment away from the UK, which is not something the government wants to see. There are also practical questions regarding its implementation and whether it will simply add another degree of complexity to an already complicated tax framework."

The UK government borrowed £34.1BN in December 2020 alone, the highest December figure on record, as the cost of pandemic support weighed on the economy.

It was also the third-highest borrowing figure in any month since records began in 1993, the ONS said.

Government borrowing for this financial year has now reached £270.8BN, which is £212.7BN more than a year ago, the ONS said.

"Fiscal policy needs to tighten only if the economy suffers long-term scarring effects that mean it is permanently smaller in the long run," Capital Economics' Dales says. "If we are right in expecting GDP to regain its pre-crisis trend, then the resulting rise in tax revenues and fall in spending means the budget deficit will drop back to 2% of GDP without the need for major tax hikes."