Image © Gov.uk

- GBP/USD spot rate at time of writing: 1.3620

- Bank transfer rate (indicative guide): 1.3238-1.3334

- FX specialist providers (indicative guide): 1.3411-1.3520

- More information on FX specialist rates here

The UK economy could be on course to recover all of its coronavirus-inspired losses as early as 2022 according to Capital Economics, although only so long as HM Treasury doesn't snatch defeat from the jaws of victory beforehand.

Britain's services-dominated economy was among the hardest hit by the 'lockdown' used to contain the coronavirus so is widely expected to enjoy one of the strongest rebounds, owing in the first instance to statistical 'base effects' but also to a so-far successful government fire-fighting effort.

The unprecedented furlough scheme has seen the government pay as much as 80% of salaries for workers at companies affected by the pandemic, enabling many jobs to be retained even as employees sat twiddling thumbs in 'lockdown' while companies' activity and turnover levels were radically curtailed.

Grants and loans to companies and individuals have also been instrumental in preventing what would otherwise have been even worse economic outcomes.

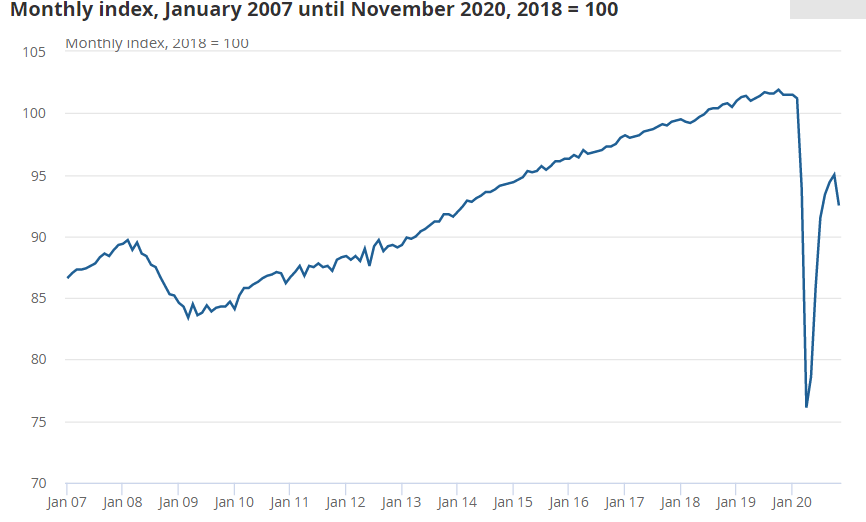

"We are more optimistic than most by expecting COVID-19 vaccines to allow the economy to surge back to its pre-crisis peak by Q1 2022 and to its pre-crisis trend in 2025," says Paul Dales, chief UK economist at Capital Economics. "Our view that people will quickly go back to the pubs/restaurants and that the economy’s supply potential won’t be permanently damaged by the crisis explains why, unlike most forecasters, we think that by 2025 GDP will be back to where it would have been had COVID-19 never existed."

Above: UK GDP index at monthly intervals. Source: Office for National Statistics.

But Chancellor Rishi Sunak and the country's accountants at HM Treasury risk snatching defeat from the jaws of victory if weekend reports from the Ft and others are right that a corporation tax increase could be announced at the March budget alongside a form of wealth.

Given the instrumental role played by HM Treasury so far it should go almost without saying that a premature curtailment of support mechanisms is a risk to the economy in the here and now as well as its recovery over the coming years. Likewise with any punitive measures like tax increases.

📢 new economics blog - why we shouldn't raise corporation tax to 'pay for Covid' 📢#Budget2021 #rishisunak #Taxhttps://t.co/Q1aLwWhFUU

— Julian Jessop (@julianHjessop) January 19, 2021

But this is exactly what Chancellor Sunak is reported to be planning for the March 03 budget, with a new personal tax that would be calculated using the value of an individual's property, pension and other assets also being mooted. Some say this would be wealth tax in all but name, like that advocated by former opposition leader Jeremy Corbyn.

“The government is rightly looking for ways to address the public deb," says Alpa Bhakta, CEO of Butterfield Mortgages Limited, which has asked 885 investors what they think of the proposals. "BML’s research shows the tax could in fact drive investment away from the UK, which is not something the government wants to see. There are also practical questions regarding its implementation and whether it will simply add another degree of complexity to an already complicated tax framework."

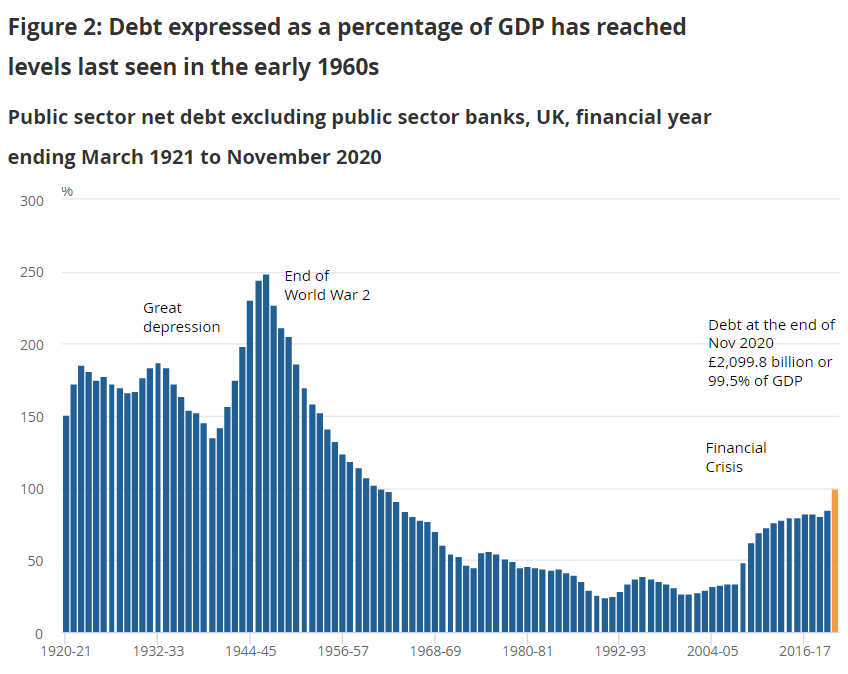

Source: Office for National Statistics.

Chancellor Sunak and the government are said to be concerned about the increase in the budget deficit and debt-to-GDP level that has resulted from Downing Street's decision to force the closure of large parts of the economy.

The budget deficit has risen sharply as a result and was running at a pace equal to 18% of GDP in November when borrowing was £31.6bn, according to Office for National Statistics data. That one-month increase in the national debt was equivalent to more than 1.5% of the UK's £2 trillion pre-pandemic GDP.

HM Treasury borrowed £240.9 billion in the first eight months of the financial year covering the period between April 01 and the end of November, demonstrating how the above monthly borrowings have become the norm since late March when the first 'lockdown' was imposed.

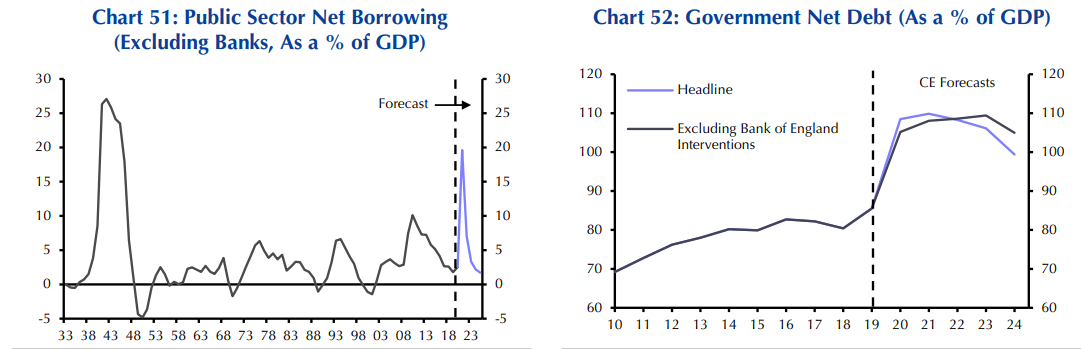

"Fiscal policy needs to tighten only if the economy suffers long-term scarring effects that mean it is permanently smaller in the long run," Capital Economics' Dales says. "If we are right in expecting GDP to regain its pre-crisis trend, then the resulting rise in tax revenues and fall in spending means the budget deficit will drop back to 2% of GDP without the need for major tax hikes."

Source: Capital Economics.

Increases in borrowing have driven the UK government's total net-debt to £2,099.8 billion at the end of November 2020, leaving it teetering on the verge of 100% of pre-pandemic GDP and no doubt playing a role in HM Treasury's thinking about the March budget.

But this isn't necessarily justification for belt-tightening at HM Treasury, not least of all because similar is true of all other economies whether major or emerging market, which means the UK and Pound Sterling are unlikely to be singled out by bond market investors for punishment or penalty.

Certainly not with the Bank of England (BoE) having bought last year, or announced a plan to buy through its quantitative easing programme this year, even more British government debt than HM Treasury has issued as a result of the attempted containment of the virus.

Furthermore, the budget deficit would fall back naturally as the economy reopens and recovers from the pandemic, which means debt-to-GDP would no longer rise at such a breakneck speed. However, this is contingent on the government not pulling the rug out from underneath companies or households in March or at any point before the economy has been allowed to reopen and afforded an opportunity to recover.

"The rebound in GDP and record low interest rates will keep the debt to GDP ratio between 100% and 110% over the next five years. So taxes need only rise if the government wants spending to be higher than before the crisis and not to fill a fiscal hole" Dales says. "In fact, an early fiscal tightening could undermine the economic recovery, lead to a permanent loss in output and create the very fiscal hole the Chancellor is aiming to fill!"