Commerzbank HQ looms over the Frankfurt skyline. Image © Andre Douque, reproduced under CC licensing conditions

The Eurozone outlook darkened in October according to respondents in the latest Leibniz Centre for European Economic Research (ZEW) survey, who flagged the coronavirus and uncertainty about the outcomes of Brexit trade talks and the U.S. election for more downbeat views on Europe's prospects.

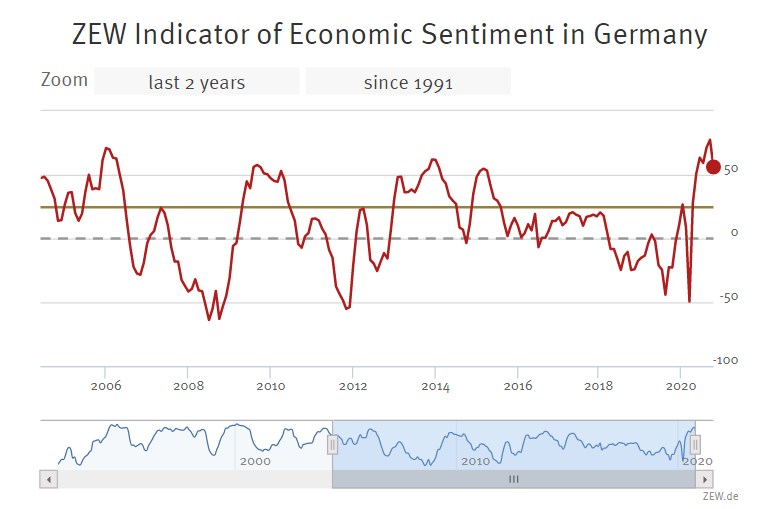

The ZEW index plummeted from 73.9 to 52.3 in October when the consensus had been for a decline to only 72.0, although the index measuring investors' assessments of the current situation rose from -80.9 to -76.6.

Meanwhile, the index measuring optimism about the six-month economic outlook for Germany also fell sharply in October from 77.4 to 56.1, although the barometer measuring the current situation rose from -66.2 to -59.5.

"The recent sharp rise in the number of COVID-19 cases has increased uncertainty about future economic development, as has the prospect of the UK leaving the EU without a trade deal. The current situation in the run-up to the presidential election in the United States further fuels uncertainty,” says Professor Achim Wambach, president of the ZEW institute. "Experts’ sentiment concerning the economic development of the eurozone also took a nosedive."

Above: ZEW expectations index.

The survey asks analysts and investors from 300 institutions including banks, insurers and financial departments of large corporations for their assessments and forecasts relating to the economic situation in all of the world's major economies but with a particular emphasis on Europe.

Expectations of the six-month outlook tumbled more heavily in Germany and the Eurozone than they did for the UK and the U.S., although the Japanese outlook deteriorated more significantly than anywhere else in the developed world.

Pessimism about the outlook has mounted after a second wave of coronavirus infections led governments to begin reimposing restrictions on activity in a number of major economies including the UK, with the most severe being implemented in Spain.

Above: ZEW expectations by country.

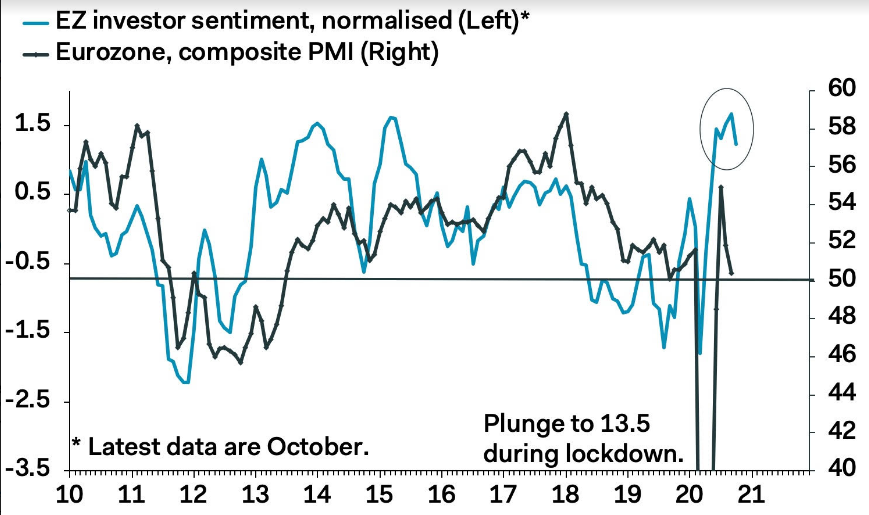

"The inevitable correction in these data now seems to be underway," says Claus Vistesen, chief Eurozone economist at Pantheon Macroeconomics. "The chart shows that our composite index of the Sentix and ZEW is now rolling over, consistent with the slide in the PMIs. More often than not, investor sentiment leads the economic surveys higher, but on this occasion it appears to be the other way around, and we fear further weakness in both, in the near term."

Europe has thus far eschewed a return to the 'lockdown' that crushed economies in the first half, instead preferring localised interventions like those announced on Monday by Prime Minister Boris Johnson, who shut pubs and some other hospitality businesses in Liverpool City region for at least four weeks.

Even more stringent measures have been taken in Spain, where bars and restaurants have been closed in Madrid and the surrounding areas while residents are unable to leave for other parts except for in certain circumstances.

Above: Pantheon Macroeconomics graph showing Eurozone investor sentiment alongside composite PMI.

Meanwhile, in Germany, nightlife is being curtailed by an evening curfew that's been implemented in Berlin while the government is widely reported to be mulling further restrictions. In addition, in the Netherlands, travel between Amsterdam, Rotterdam and The Hague is discouraged while nightlife is also curtailed by an evening curfew.

"As the colder indoor season is giving the virus more opportunities to spread, European countries will probably need more intrusive restrictions this autumn than the US did over the summer to arrest the rise in infections. Rules are likely to be tightened further in coming weeks," says Holger Schmieding, chief economist at Berenberg. "The new restrictions will curtail some economic activities in Europe. They are likely to dent consumer confidence and business sentiment with some severe damage in the directly affected sectors. Nonetheless, we expect only a temporary setback rather than a partial reversal of the recent economic progress."

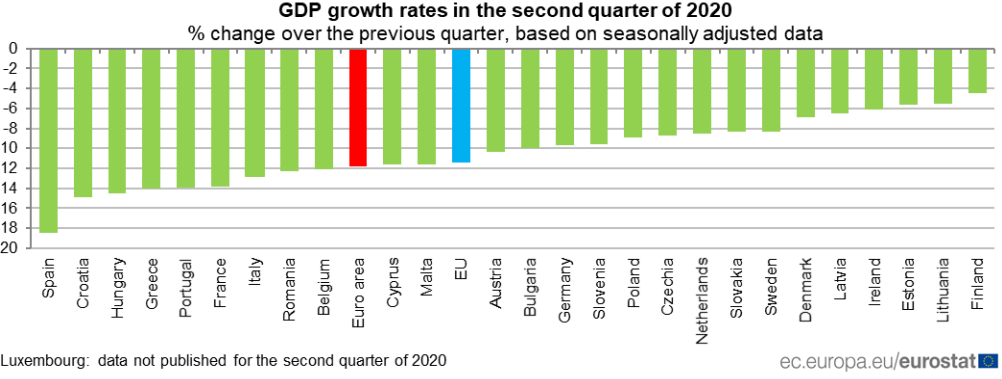

Tightening restrictions are a blow to an already bruised Eurozone economy, which shrank by -11.8% in the second quarter, a record decline that was led by a -18.5% fall in Spanish GDP. Croatia, Hungary, Greece, Portugal, France and Italy were among others that were also badly affected, with economic contractions in the double digits for each, although all now face seeing strong third-quarter recoveries suffocated by authorities' interventions.

Above: Eurostat graph showing size order of economic contractions for individual country members of the Eurozone.

But it's not just virus containment that darkened the outlook this month because uncertainty over the outcomes of Brexit trade negotiations and the U.S. election were both cited by respondents to the ZEW survey as also being behind their more downbeat outlooks for the Eurozone economy.

Brexit negotiators are attempting to reach agreement on trade terms ahead of Thursday's European Council summit, although many analysts and observers expect them to drag on until at least November amid continued differences over European demands for ongoing access to British fisheries and continued UK adherence to EU rules in a range of areas. The two sides have until December 31 at the latest to strike a deal, extend the current transition or agree to part company with no special arrangements.

Meanwhile, and although opinion polls have moved further in favour of Democratic Party candidate Joe Biden in the last week, the outcome of the U.S. election matters because Europe could potentially be on the receiving end of White House trade tariffs in the event of a second Trump presidency while China, a key trade partner for the bloc, would likely also be the target of ongoing hostilities. A Biden presidency on the other hand, is seen as likely to be more friendly toward the EU as well as China.

"Infections and the measures to contain the spread of the virus will take a toll on growth in coming months. We lower our calls for the gain in Eurozone GDP in Q4, from 1.5% to 1.0% qoq. Before the onset of the second wave of infections, we had expected 2.4% qoq for Q4. We now project virtual stagnation for Spain (0.1% qoq) and a mere 0.5% qoq gain for France," Schmieding says.

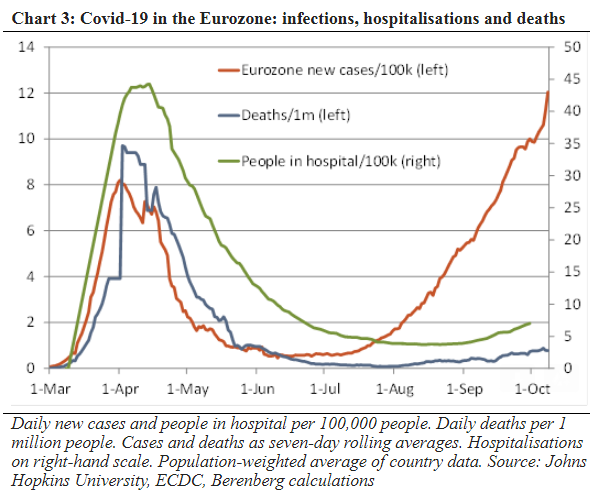

Source: Berenberg.