- CHF steady after SNB notes stabilising inflation outlook.

- As global growth, CHF's losses arrest inflation declines.

- But downside risks to inflation put floor under USD/CHF.

- Sees CHF outlook tied to EUR/USD recovery prospects.

Image © Swiss National Bank.

- GBP/CHF spot rate at time of writing: 1.2826

- Bank transfer rate (indicative guide): 1.2432-1.2522

- FX specialist providers (indicative guide): 1.2626.1.2728

- More information on FX specialist rates here

- Set an exchange rate alert, here

The Swiss Franc was little changed against the Dollar and Pound on Thursday following the March monetary policy decision of the Swiss National Bank (SNB), which has left the outlook for USD/CHF hinged on the recovery prospects of the all-important EUR/USD and EUR/CHF exchange rates.

Switzerland's Franc was sold against commodity and growth currencies like the Australian Dollar and Pound on Thursday while edging higher against low-yielding counterparts like the Japanese Yen, Swedish Krona and Euro whose inflation and growth outlooks are less assured.

The net effect on Thursday was a mixed bag of Swiss exchange rates that reflected as much a pecking order of the disinflationary plight among central bank policymakers as it did the market's contentedness with the outcome of the latest Swiss National Bank monetary policy decision.

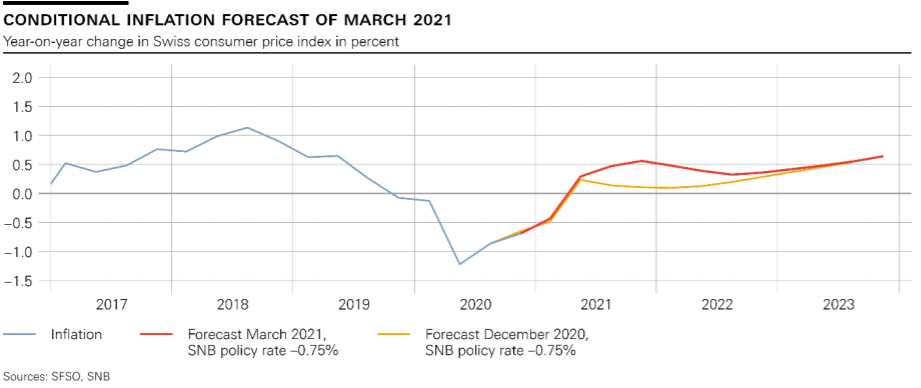

"As expected, the SNB has revised its inflation forecasts for 2021 and 2022 due to higher oil prices and the weakening of the Swiss franc. However, the revision is extremely small," says Charlotte de Montpellier, an economist for Switzerland and France at ING. "The expected rise in inflation is still low."

Source: SNB.

The SNB said in its latest assessment that economic activity is likely to return to its pre-crisis level in the second half of 2021 but that output would remain below its potential at both domestic and global levels for some time to come, reflecting challenges that long predate the coronavirus crisis. In the interim; “the pandemic is continuing to have a strong adverse effect on the economy.”

The prospect of a 2021 return to pre-pandemic levels of activity is hinged on the assumption that coronavirus containment measures are eased further in the months ahead and are not renewed thereafter, which speaks of the downside risks to inflation rates that lurk along the path ahead and make a self-defeating exercise of any meaningful upward moves in Swiss exchange rates.

Swiss exchange rates have fallen substantially in the last year as the prospects of the global economy improved, although it was largely because of these declines that the outlook for Swiss inflation has also improved tentatively in recent months. Without them, the SNB's policy stance could have been somewhat different this Thursday.

"This morning’s decision by the Swiss National Bank to keep its policy settings unchanged came as no surprise. The prospect of further falls in the franc should allow the Bank to largely stay out of the FX market, but the policy rate will remain rooted at a record low," says David Oxley at Capital Economics. "Indeed, while the Norges Bank’s attention has shifted to rate hikes, SNB Chairman Thomas Jordan couldn’t have been any clearer in saying that there is “no signalling at all for a change to monetary policy.”

Source: SNB.

SNB policymakers left Switzerland's main interest rate unchanged a -0.75% on Thursday, the lowest in the world, and said they willing to intervene in the currency market to weaken Swiss exchange rates "as necessary." This was a slight and subtle change of guidance from the previous warning that the bank would intervene "more strongly" if necessary, which indicates a degree of satisfaction with recent developments and one that could see less intervention from the SNB in the coming months.

But a lesser inclination toward intervention indicates merely reduced downward pressures on Swiss exchange rates, rather than any signal of upside potential for the currency and speculatively minded participants in the market. Any such upward momentum in the Swiss Franc would be entirely self-defeating because of the erosive impact it would have on the tentatively improved inflation outlook that was acknowledged by the Swiss National Bank this Thursday.

Central banks use interest rates and other monetary policy tools including quantitative easing and foreign exchange market intervention in order to manage inflation pressures such that they're consistent with statutory mandates and preset targets. The policy playbook would typically see excessive inflation pressures curbed by either higher interest rates, lesser bond purchases or FX intervention to strengthen exchange rates and vice versa.

“My view is that we have entered a period of low vol consolidation where US rates stop going up for a few weeks and everything stabilizes as we process the new higher level of global rates,” says Brent Donnelly, a spot FX trader at HSBC. “This probably means that USDCAD is a sell up here as we approach the post-COVID down trendline (currently 1.2626). Look for USDCHF and USDJPY to range trade for a while with a modest downside bias.”

Above: USD/CHF shown at daily intervals with EUR/CHF (orange) and GBP/CHF (purple).

In a world of low-to-no inflation exchange rate trends can have meaningful impacts on central bank policymakers and their ability to meet targets that exist for reasons of macroeconomic and financial stability. Switzerland has typically suffered from exchange rates that are too high, which act to cheapen the price of imported goods and in the process undermine the 2% annual price growth the SNB is charged with delivering.

This has important implications for what is or isn’t more likely in the evolution of Swiss exchange rates, such that a meaningful move lower in USD/CHF would only become possible in a market where EUR/CHF is moving higher to offset increases in the trade-weighted Swiss Franc.

The latter is more-than one half composed of the Euro while only one tenth interested in the U.S. Dollar, which means that declines in EUR/CHF would need to be met by a factor of five or more in USD/CHF in order for them to be offset in the trade-weighted index and vice versa.

The most important implication of this is that USD/CHF falls could only be sustained in the event of a Euro-Dollar rate recovery that is able to lift EUR/CHF, which leaves the outlook for Swiss Franc strength and those bullish on the currency hinged entirely on a reflation of the single currency.

“The economy of Switzerland has shown more vigour than most of its neighbours in the euro area since 2H of last year but that will not lead the SNB to drop its guard and dovish policy bias at today's meeting,” says Carole Laulhere, a strategist at Societe Generale. “EUR/CHF broke out above an ascending triangle paving the way for short-term uptrend. It has witnessed an initial pullback however 1.1000, the 38.2% retracement from February has provided support. Once the pair can establish itself above the short-term descending channel near 1.1100, the uptrend is likely to resume towards 1.1180 with possibility to reach projections of 1.1250/1.1280.”

Above: USD/CHF shown at monthly intervals with EUR/CHF (orange) and GBP/CHF (purple).