- Pound to Canadian Dollar exchange rate: 1.6770

- US Dollar to Canadian Dollar exchange rate: 1.3276

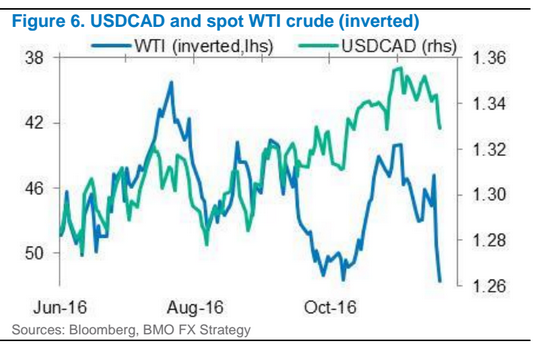

The main driver for CAD in the week ahead will be oil prices - rather than yield differentials - says Stephen Gallo of BMO Capital Markets.

Since OPEC’s decision to cut supply last Wednesday oil has taken over as the primary driver of the Canadian Dollar.

While many market-watchers have long assumed that the oil price and Canadian Dollar go hand-in-glove this is not actually always true.

Indeed, over recent months the ability of oil to move CAD has waned particularly as oil prices settled into a range between 40-50 dollars a barrel.

But, since the OPEC meeting WTI crude oil has breached the 50-level indicating it could be about to break out of the range.

Stephen Gallo, at the Bank of Montreal, says a breakout from the range would re-connect the two assets which so often move in tandem:

“CAD gained 1.7% against the USD last week and 1.6% on a trade-weighted basis.

"The gain came as WTI crude rallied from $46 to $51 on the back of the OPEC decision.

“When oil is bouncing around in a tight range, it tends to lose its influence on USDCAD.

"But the breakout above the $40-50 range is a game changer,” said Gallo.

Some analysts think the break higher could lead to a move up to as high as 60 dollars a barrel, and in such a circumstance the Canadian dollar would also rise sharply.

The importance of oil prices were laid bare in the country's most recent statistics on trade.

The Canadian trade deficit narrowed by over $3 bn in October in reaching $1.1 bn, as higher oil prices, and a more normal track to imports helped the balance recover from record-wide levels in September.

"A single shipment related to the Hebron oil project was responsible for $2.9 bn of the now-revised $4.4 bn September deficit. In October, the narrowing from the adjusted baseline, which excludes that mammoth piece of equipment, was driven by firmer prices - particularly for oil - as export volumes declined on the month," says Nick Exarhos at CIBC Economics.

Therefore, even if the trade balance looks to be in much better shape for October, the GDP outlook isn’t off to the best of starts and we would presumably need to see further climbs in oil to get the economy to step into an higher gear.

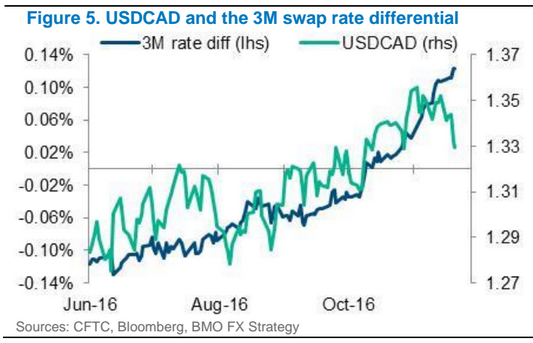

Yields Lose influence

The rising importance of oil has pushed the other major driver for the Canadian Dollar - the differential between three-year bond yields in Canada and the United States - into second place.

Three-year yields reflect medium term inflation expectations and therefore interest rates set by central banks.

Investor capital tends to flow from the lower yield/interest rate currency jurisdiction to a higher interest rate currency.

The chart below shows how the difference – or spread – between the three-year US and Canadian three-year bond yield has risen sharply recently.

However, over recent days the linkage has snapped.

The sudden negative correlation is due to a new factor offsetting the influence of yield differentials: the rising price of oil.

Higher oil prices have supported the Canadian Dollar despite pro-USD yield differentials.

Latest Pound / Canadian Dollar Exchange Rates

| Live: 1.8824▼ -0.37%12 Month Best:1.9044 |

*Your Bank's Retail Rate

| 1.8184 - 1.8259 |

**Independent Specialist | 1.856 - 1.8636 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

BOC To Deliver Marginally Dovish Message

The main event on the economic calendar this week for the Canadian Dollar is the Bank of Canada (BOC) rate meeting on Wednesday December7.

Recent GDP data was surprisingly positive and beat BOC forecasts leading to a more upbeat assessment of the economy.

However, borrowing rates have risen strongly due to Trump reflation, and unlike the US Canadian’s cannot afford higher borrowing costs.

One way to cool rates would be for the BOC to talk about cutting rates.

The improved data, however, makes it unlikely they will be able to talk directly about a rate cut at their meeting.

CIBC Economics’ Avery Shenfield, says the bank will have to walk something of a tightrope in their statement, “having stood pat in October, and seen data slightly top its projections since then, the Bank wouldn’t be able to credibly claim that it seriously considered a rate cut in December,” says Shenfield.

“So the Bank will simply have to clear its throat and remind the market that a tightening in financial conditions (i.e., higher bond yields) isn’t welcome, perhaps just by drawing attention to it.

“Emphasizing that the output gap won’t be closed for a considerable period will be a reminder that there’s still an outside chance of a cut,” added the CIBC analyst.