- BoC decision due Wednesday

- Comes amidst CAD underperformance

- CAD at risk of 'dovish' comments

- Barclays remain constructive

Above: BoC Governor Macklem. Image © Bank of Canada, Reproduced Under CC Licensing.

- GBP/CAD reference rates at publication:

- Spot: 1.7276

- Bank transfer rates (indicative guide): 1.6670-1.6792

- Money transfer specialist rates (indicative): 1.7120-1.7150

- More information on securing specialist rates, here

- Set up an exchange rate alert, here

The looming key risk for the Canadian Dollar will be the midweek Bank of Canada policy decision where it is expected another cut to the quantitative easing programme will be announced.

Markets look for the Bank of Canada (BoC) to cut its bond purchases from $3bn/week to $2bn/week owing to the strong economic recovery,

What does the decision mean for the Canadian Dollar?

Firstly, a further scaling back of the quantitative easing programme (a process known as tapering) is largely expected therefore it is unlikely to have a material impact on Canadian exchange rates in isolation.

However, there will be numerous 'moving parts' to the BoC's communications and this could be where some CAD-moving surprises are thrown up.

"While tapering seems widely expected next week, the tone from the meeting or inflation forecast revisions in the MPR could result in some reaction from CAD," says Zach Pandl, an economist at Goldman Sachs.

Perhaps the biggest surprise would be an unexpected decision to keep purchases unchanged as Governor Tiff Macklem nods to rising expectations for slowing global economic growth rates in response to the spread of the Delta variant.

Such a surprise could undermine the Canadian Dollar but is unlikely to transpire given robust domestic data and the BoC's previous guidance.

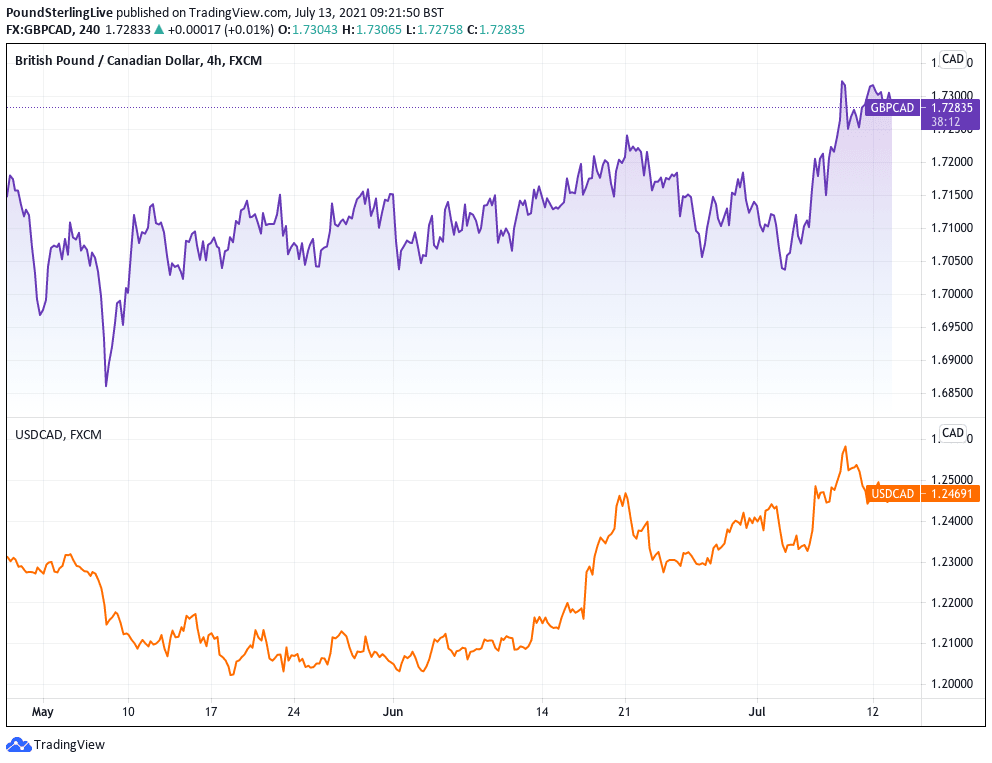

The BoC event comes as the Canadian Dollar extends a short-term trend of weakness that has seen it lose ground to both the Pound and U.S. Dollar:

Above: Four-hour chart showing GBP/CAD (top) and USD/CAD (bottom).

Recent declines in the Canadian currency come amidst a softening in global investor sentiment and despite the BoC being one of the more 'hawkish' major central bank - i.e. one that is ahead of its peers when it comes to normalising interest rates to pre-crisis levels.

This is particularly true with regards to GBP/CAD and USD/CAD, given the BoC is expected to both taper quantitative easing and then raise interest rates ahead of the U.S. Federal Reserve and Bank of England.

The BoC's 'first mover' stance would typically be expected to convey a degree of support to the Canadian currency.

Exchange rate trends therefore suggest that the taper has long been expected by markets and is therefore in the existing valuation of the Canadian Dollar.

This means the BoC will have to taper just to keep the currency at current levels.

Indeed, the BoC could in fact struggle to meet the market's lofty expectations and any 'dovish' turn could be met with Canadian Dollar sales.

"We are in waiting mode for the BoC tomorrow, looking for a further taper but with a high hurdle for a hawkish surprise given 2022 pricing for hikes," says Elsa Lignos, Global Head of FX Strategy at RBC Capital Markets.

Money market pricing shows investors to now be expecting a first interest rate hike early in the second quarter of 2022.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

Economists at Barclays expect the BoC to keep its forward guidance on rates unchanged: slack is expected to be absorbed, and inflation is consequently expected to return to the target on a sustained basis sometime in the second half of 2022.

"We think that the bank could continue to reduce the pace of purchases by CAD1BN each quarter, which would stop net purchases by year-end or early 2022. We expect the BoC to start hiking in H2 2022, in line with forward guidance," says Marek Raczko, an analyst with Barclays.

The BoC will feel justified in reducing the support it offers the economy owing to recent data releases that have come in ahead of expectation.

Canada's June jobs report surprised to the upside when it read at 230k, which was ahead of the consensus forecast for a reading of 175k.

This means the economy has recovered close to 84% of the jobs lost to the third wave in April and May.

"We expect that the solid June jobs report and strong survey data, as well as the improved public health situation will lead the BoC to taper asset purchases further," says Pandl.

Canada's GDP fell by 0.3% in April, which is better than the -0.8% reading the market was expecting.

The BoC's Business Outlook Survey released last week meanwhile showed a continued improvement in business sentiment and broadening of the recovery ahead with firms tied to high-contact services becoming more confident that sales will pick up.

Money market pricing shows the market is now expecting a first interest rate hike early in the second quarter of 2022, which is at odds with Barclays' and Goldman Sachs' expectation for that hike to come a little later.

"BoC hawkishness seems to be well priced-in so the announcement of another leg of tapering might not generate significant market reaction," says Raczko.

"In the near term, the loonie remains vulnerable to oil price volatility and broader risk sentiment, but has lagged the interest rate differential, which moved in favour of Canada," he adds.

In the medium-term, Barclays remain constructive on the Canadian Dollar owing to solid domestic fundamentals, still supported oil prices on global demand recovery and a hawkish BoC.

Goldman Sachs tell their clients they expect the first BoC interest rate rise too one in the second half of 2022, although they conceded risks are skewed toward an earlier hike.

Goldman Sachs continue to see further upside for Canadian Dollar exchange rates on a 12-month horizon.