The underpinnings of the current uptrend are likely to be eroded as 2018 progresses leading NAB to keep their forecasts for the Aussie Dollar bearish.

The Australian Dollar's recent rally has been built on a combination of factors, including rising commodity prices, M&A flows, demand for bonds and rising risk appetite, but will it last?

Probably not, thinks Ray Attrill, Head of FX Strategy at National Australia Bank (NAB), who says the factors underpinning the recovery aren't likely to persist in 2018.

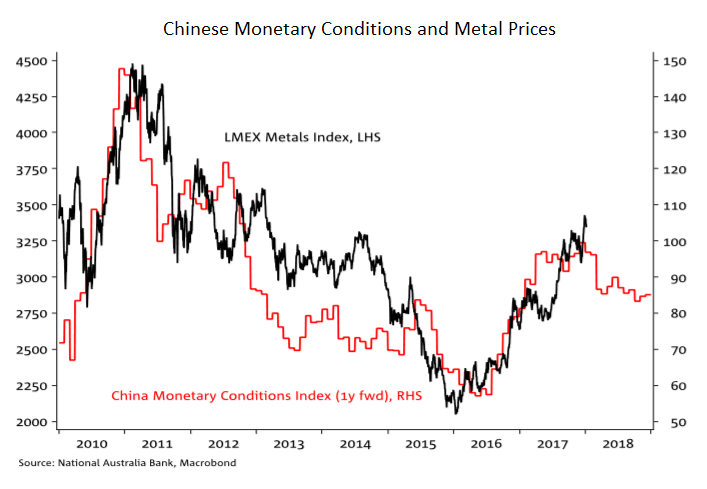

Recent rises in the price of metals such as Copper, Lead, Zinc, Silver, and Iron have all supported the Australian Dollar because Australia is such a major producer and exporter of these metals.

A major factor in the commodity rally is strong global growth because developing countries tend to be especially resource hungry.

China, in particular, is a big consumer of commodities, especially Australian commodities, and it too is showing above-expectations economic resilience.

"The broadening of the global growth recovery, evident in the healthy December PMI readings across the globe, has undoubtedly been a factor supporting commodities with China’s readings in particular (both the official and Caixin PMIs) surprising on the upside despite concerns for a potential pullback," says Attrill.

China's newfound drive to cut levels of pollution by favouring higher grades of iron ore has favoured Australian ore in particular because it is of a higher grade and therefore less harmful to the environment.

The rally in commodity prices is more likely than not to continue in January, says Attrill, because there is a strong seasonal bias to commodity prices doing well in the first month of the year.

"Seasonality is also supportive of further commodity price gains in January. The CRB index has a tendency to rise at the start of the year. The Bloomberg heat map shows positive returns in eight of the last ten Januarys. If history repeats, the AUD is likely to continue drawing support from commodity prices in coming weeks." Notes the analyst.

Beyond January, however, and NAB are sceptical of commodities continuing their uptrend.

Commodity prices are highly correlated to monetary conditions in China, or the supply and cost of credit.

When those monetary conditions tighten as is currently happening, demand for commodities tends to fall as borrowing becomes more expensive and investment in commodity-rich heavy industries stalls.

"Looking further out, we still contend that commodities will be less AUD-supportive over the course of 2018. The relationship between China’s growth and commodities demand versus China’s monetary conditions works with a lag and the full impact of tighter conditions over the past few months have not yet worked through." Says Attrill.

Another factor which could also reduce commodity prices and hit the Australian Dollar is the possibility of commodity over-supply.

"Supply dynamics are also a consideration, particularly for iron ore and metallurgical coal. On this score, we share the view recently published by Australia’s Department of Industry, Innovation, and Science which notes the upcoming increase in output will likely weigh on prices. "

Demand for Australian Bonds

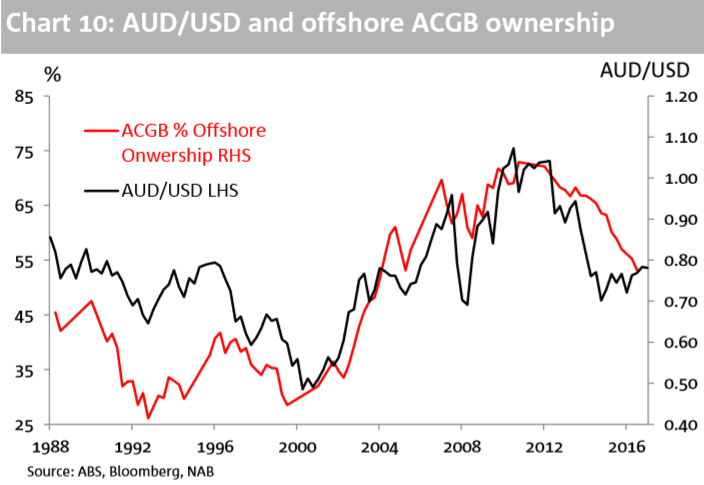

Foreign investor demand for Australian corporate and government bonds (ACGB) has always been a strong driving factor in demand for the currency and therefore its appreciation.

The chart below shows the percentage of foreign ownership of ACGBs overlaid with the AUD/USD exchange rate and the high degree of correlation is especially noteworthy.

Yet Attrill is not particularly optimistic about demand for Aussie bonds being sustained, particularly, as rising interest rates in the US and 'rest of the world' (RoW) may make US Treasuries and emerging market debt a more attractive option for investors.

On the flipside, an improvement in global growth will probably be supportive for the Aussie as it tends to benefit from rises in risk appetite.

M&A Flows

The impact of large mergers on the FX market can be significant, and this appears to be the case over the last month, according to NAB.

"We suspect corporate-related FX flows in a low-liquidity pre-Christmas environment has been the opposing and dominant flow influence," says Attrill.

Several high profile takeovers will mean increased demand for Australian Dollars by foreign companies taking over Australian corporate targets.

"On December 13 Unibail-Rodamco, a European owner of shopping malls, announced the agreement to buy Westfield for A$32.7bn, 35% of which will be paid in cash. While the deal won’t likely close until mid2018, hedging of at least some of the cash proceeds back to AUD likely occurred in December. The day before the Westfield announcement, Zurich Life also announced that they would buy ANZ’s Australian life insurance business for A$2.85bn," says Attrill.

It's not clear, however, whether this particular driver will be a short-term dynamic for forex or a medium-term influence, given the official takeover date for Westfield is not until the middle of 2018.

It could indicate increased flows from this source during most of the year as dealers tend to stagger FX transactions for large M&A's over a fairly wide period of time.

Get up to 5% more foreign exchange by using a specialist provider by getting closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here.