Contradictory opinions concerning the outlook facing the Australian dollar suggest the AUD/USD could trade anywhere between 0.77 and 0.67. Whose argument is more compelling?

The GBP to AUD exchange rate is at 1.9183 and continues its trend lower. For this pair it's not worth discussing research and projections until the outcome of the June 23rd vote is made clear.

However, we can still assess the Australian dollar's outlook against other less volatile currncies, such as the greenback.

The AUD to USD exchange rate is currently hovering around 0.7380, around the initial highs following the Reserve Bank of Australia (RBA) event last week.

It is approaching near-term technical resistance points that could see gains capped at the 0.7400-0.7380 level.

Concerning the longer-term outlook, this Australian dollar strength can be traced back to the dollar’s home-spun woes.

The most recent US payrolls report all but ended the chance of the Federal Reserve tightening this month, triggering a sharp move higher in AUD/USD.

This is because markets now see the higher yield offered by Australia as likely to hold its advantage for a while longer.

The RBA's cash rate is at 1.75%, the Fed’s base rate is at 0.5% - the idea is that you borrow in US dollars and save in Aussie dollars - the demand drives up the AUD/USD and has been doing so since the financial crisis.

The rebound in AUD extended after the RBA left interest rates unchanged at its latest monetary policy meeting - i.e investors see higher rates in Australia lasting for longer.

Latest Pound / Australian Dollar Exchange Rates

| Live: 1.9276▲ + 0.14%12 Month Best:2.1005 |

*Your Bank's Retail Rate

| 1.8621 - 1.8698 |

**Independent Specialist | 1.9006 - 1.9083 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

As a result of the convergence of policy expectations, the currency pair is now at a mid-range level around 0.74.

Lloyds Bank have struck a positive tone concerning the Australian dollar’s outlook in their latest monthly forecast note.

Lloyds base their positive stance on recent Australian data having been strong – the unemployment rate (5.7%) and Q1 GDP (3.1% on an annualised basis) were both stronger than consensus and the trade deficit narrowed substantially (from A$2.2bn to A$1.6bn) – underpinning RBA Governor Steven’s more upbeat tone recently.

The RBA sounded a positive tone at their June policy meeting and failed to include an explicit easing bias their statement, which has stirred confidence amongst the Aussie bulls.

This implies a rate cut in July is almost certainly off the table.

“While inflation remains muted, and poses a risk of additional policy loosening from the RBA, we believe economic data will remain robust and forecast AUD/USD to climb towards 0.77 by end-2016,” say Lloyds

The Opposing Views: The Australian Dollar is Forecast Below $0.70

Highlighting just how tricky it could be to navigate the Aussie dollar market place, Societe Generale have confirmed they do not share Lloyds' positive view on the longer-term outlook for the Australian dollar.

In their latest ‘6 month ahead’ forecast note Soc Gen’s Alvin Tan tells us that “the fundamental backdrop for the Australian dollar remains challenging.”

There is a notable contrast to the upbeat view Lloyds hold on the country’s fundamentals.

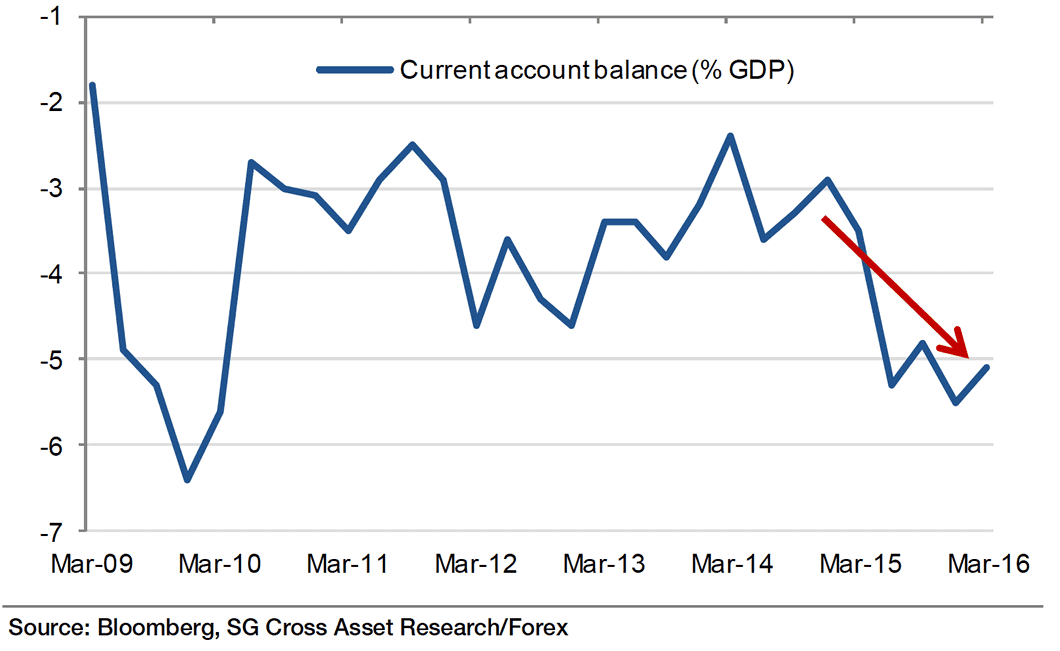

Tan argues that the Australian economy is gradually transitioning away from the natural resource sector, aided by low interest rates and a weaker currency, but the current account imbalance has widened in recent quarters.

Above: A deterioration in Australia’s Current Account has been observed of late

“Non-mining capex growth has been elusive, the RBA is firmly on a dovish policy setting, FX market implied volatility is elevated, Fed policy normalisation remains on track and risks to the Chinese growth outlook abound,” argues Tan.

It is observed that the Australian terms of trade is still falling, “and thus the fundamental path of least resistance for AUD is for further depreciation.”

This, plus the persistent and surprising disinflationary pressures in Australia, has kept the RBA on an easing bias, with one rate cut expected in H2 16.

Monetary divergence should thus be another factor in the second half of the year for a lower AUD/USD as the Fed readies to tighten again.

Societe Generale are forecasting the Australian dollar to end 2016 at 0.65, ahead of a gentle recovery towards 0.67 in March 2017.

It is not just Soc Gen who are bearish on the Australian dollar.

Analysts at Morgan Stanley and ANZ have confirmed they see a softer path for the Aussie dollar through 2016.

ANZ say they see potential economic growth in the country at 2.5%, below the 3% rate commonly assumed.

“While in the near term this has few implications for the AUD, over the medium term the impact is large,” say ANZ.

If potential growth has indeed fallen, it means that the neutral cash rate at the Reserve Bank of Australia must also be lower.

“It means that in the near term cash rates are not as stimulatory as we previously thought, and as such the risk of further easing remains. While second, in the longer term, it means that the overall rate structure in Australia will be lower, and as such Australian rates will continue to converge on global rates,” say ANZ.

Morgan Stanley's Charles Rubenfeld says he remains bearish AUD and looks to sell AUD rallies as he expects the RBA easing to push AUD lower.

"However, we still believe the RBA will eventually need to react to the worrying inflation trend and still vulnerable external accounts and our economists are now expecting another 75bp of rate cuts," says Rubenfeld.

Who to Believe?

With the Fed striking a steady hand at their June FOMC meeting we can see a steady rate rise path ahead and would argue the USD is looking neutral at present.

The three analysts cited in this piece rest their cases with expected RBA action.

It therefore falls to the Australian economy to convince us that it does not need further stimulatory assistance from the RBA.

The most recent data at hand - Australian labour market figures - shows the employment situation remains in good shape.

The May labour force report showed ongoing solid employment growth with 17.9K people finding work, ahead of consensus forecasts for 15K.

Furthermore, a number of indicators are now providing a more consistent picture of continued strength in the labour market, pointing to further solid jobs growth.

"For the RBA, today’s numbers are encouraging, but, on balance, we expect that persistent weakness in inflation will be enough to see the Bank cut the cash rate again in August," say ANZ Research in their assessment of the data.