- GBPAUD now technically oversold

- Looking for consolidation

- AUD under pressure at start of new week

- As Chinese property stocks slump

Image © Adobe Images

The Pound to Australian Dollar exchange rate (GBPAUD) looks set to consolidate after the recent selloff left the pair at oversold levels, particularly if renewed fears concerning Chinese property stocks persist.

The Pound has been under broad-based pressure over the past month as markets slash expectations for the amount of interest rate hikes to come from the Bank of England, culminating in last week's sharp selloff following the Bank's decision to hold rates unchanged.

The Australian Dollar has meanwhile been better supported against a host of currencies amidst an improved sentiment towards China (peak pessimism has passed) and some solid domestic releases that maintain expectations for another Reserve Bank of Australia (RBA) interest rate hike.

The net result is a fall in GBPAUD of nearly 5% from its August peak to around 1.9060, where we find it today.

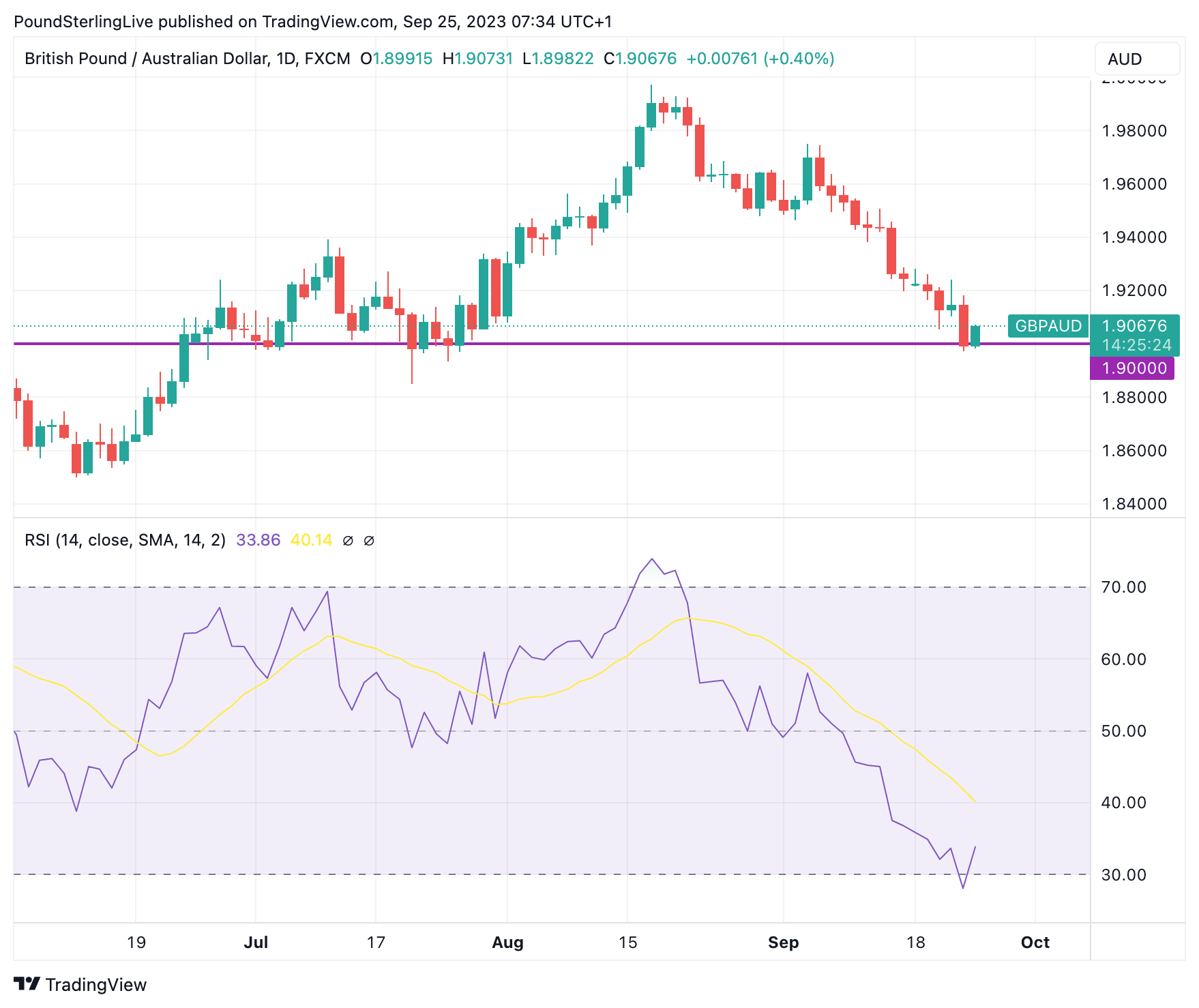

The pace of the decline has meant the exchange rate is left looking oversold on a technical basis, signalled by the Relative Strength Index (RSI) sliding below 30, as can be seen in the lower pane below:

Above: GBPAUD at daily intervals with the RSI in lower panel.

The RSI is a momentum signal that has an important benefit in indicating when a move is getting too extended. For the RSI to correct, a period of consolidation or recovery in GBPAUD would be required.

The above chart also signals an area of support located near 1.90, confirming that daily closes below here have not been held for a number of months.

This support level coincides with the overextended RSI, creating a neat technical narrative that this is an exchange rate ready to consolidate.

The Australian Dollar was under pressure at the start of the new week amidst fresh worries over China's property sector, a key source of Chinese economic underperformance and AUD weakness during 2023.

It was reported Monday that Chinese property stocks tumbled the most in nine months as concern over a possible China Evergrande Group liquidation added to fresh signs of stress across the industry.

Evergrande - the mega-developer - dived 25% after it scrapped key creditor meetings at the last minute and said it must revisit its restructuring plan.

China Aoyuan Group Ltd. was however the biggest faller, slumping by a record 76% after shares resumed trading.

Chinese property is a key driver of global iron ore and raw material demand, which matters for Australia's export earnings. "Adding to pressure on the A$, China’s sluggish growth and investor concerns over the property and financial sectors look set to persist. We expect short-covering rallies at times but the trend into September is likely to remain downward," says Imre Speizer, a strategist at Westpac.

Expect sentiment towards China to be the major driver of AUD this week, given the relatively quiet domestic calendar in Australia.

Of interest, however, will be the release of the weighted mean CPI on Wednesday, which gives a near-term indicator as to how inflation is evolving. The consensus is for a 5.2% reading.

Australian retail sales are due on Thursday, where consensus looks for a print of 0.5%.

Image © Adobe Images

The Pound could meanwhile struggle given the downturn in momentum related to the Bank of England's decision to halt its interest rate hiking cycle amidst slowing inflation and economic activity.

In the UK, Friday sees the second release of Q2 UK GDP data, meaning the likely market impact of the numbers will be minimal.

Markets are nevertheless looking for GDP growth in Q2 to be at 0.4% year-on-year and 0.2% quarter-on-quarter. Any major deviations could offer some short-term volatility.

Note that revisions will also be made to previous data for 2022 and 2023. This is "particularly pertinent now that the ONS has indicated huge revisions to data for 2020 and 2021 that have altered history quite considerably," says Philip Shaw, an economist at Investec.

The ONS has updated its measure of UK GDP by incorporating a wider range of improvements to sources and methods to measure output. It says the new methods put it at the forefront of global efforts to improve accuracy in measuring national accounts.

These improvements will now come forward into the official data. When the results of the updated model were announced it was revealed current price GDP growth for the UK in 2021 was revised up 0.9 percentage points to an 8.5% increase; this follows an unrevised fall of 5.8% in 2020.

Annual volume GDP growth in 2021 was revised up 1.1 percentage points to an 8.7% increase; this follows an upwardly revised 10.4% fall in 2020 (previously an 11% fall).

This means the UK is no longer the laggard amongst major peers in the post-Covid era.