- GBP/AUD in short-term downtrend with no signs of a reversal

- Currently penetrating through major support

- RBA & BoE decisions key up-and-coming events

Image © Adobe Images

- GBP/AUD reference rates at publication:

Spot: 1.8200 - High street bank rates (indicative band): 1.7566-1.7693

- Payment specialist rates (indicative band): 1.8040-1.8112

- Find out about specialist rates, here

- Or, set up an exchange rate alert, here

The Pound to Australian Dollar exchange rate (GBP/AUD) is trading at around 1.8189 at the time of writing after falling 1.15% in the week before; studies of the charts suggest the pair will continue falling in line with the dominant downtrend.

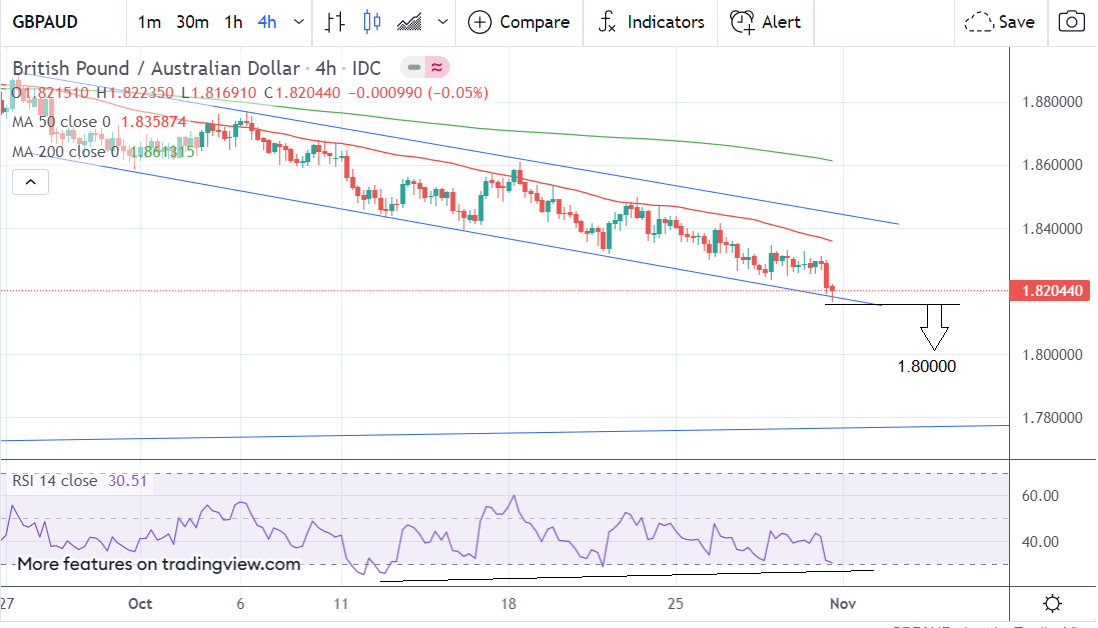

The 4 hour chart - used to determine the short-term outlook, which includes the coming week or next 5 days - shows the pair steadily descending in a series of declining peaks and troughs.

Although the trend looks 'long in the tooth' now, there are no major signs of reversal so the bias is for it to continue.

The only minor sign suggesting the bear trend may be reaching a conclusion is the RSI indicator in the bottom pane which is converging slightly with price.

The RSI has not properly entered oversold territory since the 11th of October, suggesting bearish momentum is waning, however, on its own it is not enough to indicate the downtrend is about to end.

Above: Four-hour chart for GBP/AUD.

In trying to determine a potential short-term downside target for GBP/NZD, the 1.618 Fibonacci ratio extension of the previous move offers the 1.8000 level offers a key objective.

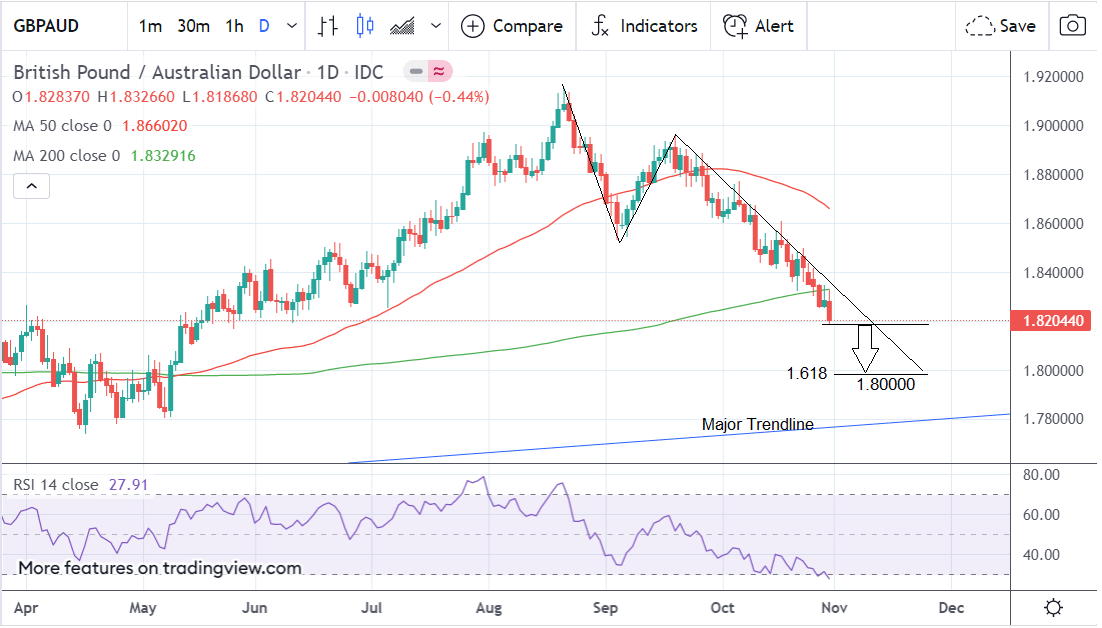

The pair has gained bearish momentum after piercing through all of the three major long-term averages it was sitting above last week. These include the 200-day, 200-week and 50-week Moving Averages.

With all these now breached the downtrend will gain credibility and followers.

Above: Daily GBP/AUD chart.

The daily chart shows the pair is in a short-term downtrend which, in the absence of any signs to the contrary, is likely to extend.

On the daily chart it is possible to see more clearly how the 1.618 Fibonacci extension provides us with a downside target.

It is calculated as a multiple of the initial move from the August highs to the early September lows.

The daily RSI is not converging but it is in oversold territory. Welles Wilder, the originator of the indicators said this was a signal to stop shorting the market. If the RSI exits oversold, it will be a signal to go long.

The daily chart shows how the trend could play out over the medium-term, or next week to month.

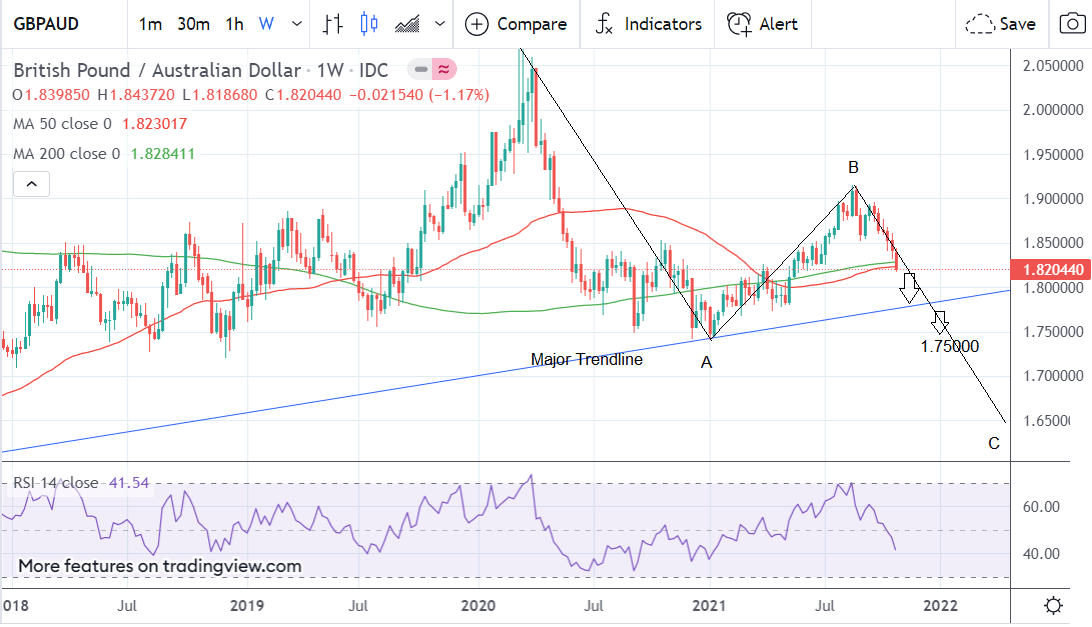

Above: The long-term weekly GBP/AUD chart.

The weekly chart - used to give an idea of the longer-term outlook, which includes the next few months - is showing a more bearish picture for the pair.

For starters, it is showing how the pair has recently pierced through two major moving averages, the 50 and 200-week MAs. It did this last week and, importantly, then closed the week below them. This suggests fairly definitive penetration has taken place.

A re-break below the lows of the week could now also signal a continuation of the bearish trend and last week’s long red marabuzo candlestick is another bearish continuation signal.

Further, the steep descent from the March 2020 highs is a bearish sign. The lack of strength in the up move that launched itself in January 2021, suggests bears appear to be in control longer-term.

We also note what could be a large measured move pattern forming beginning with wave A going down from the Mar 2020 highs, wave B encompassing the move up from the Jan lows and possibly wave C starting with the move down from the August highs at 1.9154.

If this is the case, it could indicate a much more bearish long-term outlook for the pair, with the potential for a bear trend to take the exchange rate down to circa 1.6000 eventually.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

The Australian Dollar: All About the RBA

The key data release for the Aussie Dollar in the week ahead, is the Reserve Bank of Australia (RBA) interest rate decision at 3.30 GMT on the morning of Tuesday, November 02.

After that, the actual monetary policy statement from the meeting will be published five days later on November 5.

The actual interest rate decision on November 1 is unlikely to show a change in the cash rate from the current 0.1%.

The RBA has said that it sees current inflationary pressures as purely transitory and does not intend to lift rates until 2024.

What will be more heavily scrutinised is the actual policy statement released on Friday, as this will contain the bank’s updated forecasts.

Last week’s inflation data showed a higher-than-expected uptick in the RBA’s Trimmed Mean CPI for the third quarter, which came out at 0.8%, beating the forecast 0.5% rise.

The RBA gauge is considered a much more accurate picture of the real level of inflation compared to official data, since it provides a better picture of the longer-term trend. Whilst the beat is, therefore, significant it is unlikely to radically change the outlook long-term bank policy expectations.

Should the bank’s forecasts in its statement suggest inflation is becoming a greater concern for the board, however, the Aussie could rise on expectations of a foreshortened timeline to normalising interest rates.

The Pound: All About the Bank of England

Further potential for any substantive moves in GBP/AUD would likely only come in the wake of the Bank of England policy decision, due Thursday mid-day.

The Bank could raise interest rates by 15 basis points, a decision that has been anticipated by investors for much of the past month according to money market pricing.

Faced with surging inflation members of the Bank's Monetary Policy Committee (MPC) have spoken about the need to raise rates in order to ensure inflation expectations amongst businesses and consumers do not start running higher.

The decision to raise rates would therefore be in keeping with the Bank's key role of guarding price stability in the economy.

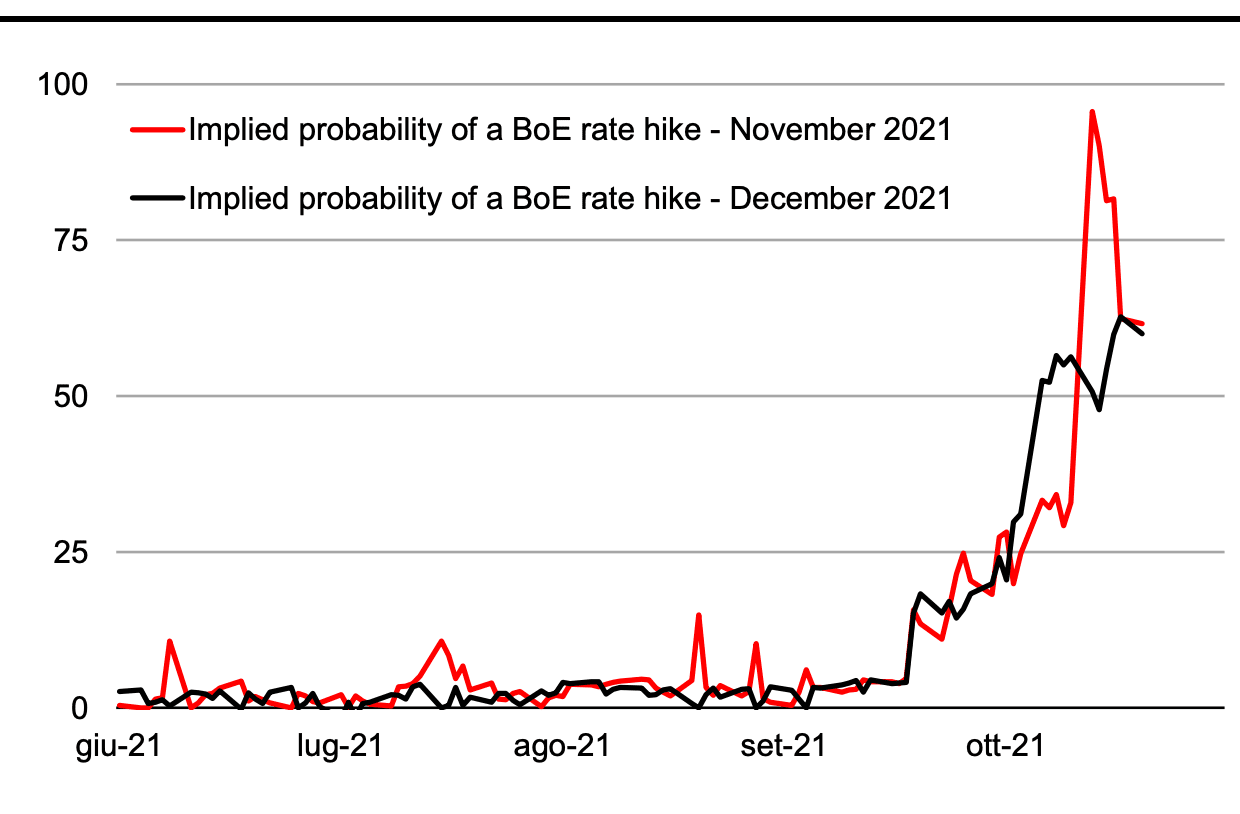

It is however worth bearing in mind that the odds of a November hike have fallen over the duration of the last week while the odds of a December rise have increased, according to money market pricing:

The repricing in favour of a December rate hike over recent days might go some way in explaining why the Pound to Australian Dollar exchange rate continues to face downside momentum.

"The probability of a November hike, which jumped to 100% following the hawkish turn by the BoE early this month and tough remarks by BoE Governor Andrey Bailey and other MPC members, has now converged with the probability of a move in December," says Roberto Mialich, a foreign exchange strategist at UniCredit.

Above: "A BOE RATE HIKE EITHER IN NOVEMBER OR DECEMBER IS EQUALLY PRICED INTO THE UK OIS CURVE" - UniCredit.

Waiting for December will be preferred by some members of the MPC as they will have received the full suite of official labour market data since the ending of the government's furlough scheme in September.

This will give policy makers a clue as to just how robust the labour market is and also suggests the November labour market report (due Nov. 16) could perhaps be the single most important event in the remainder of the year for Sterling.

A better than expected labour market report could give the MPC the cover required to move on rates in December, while a softer than expected outcome could provide enough hesitation to push any rate hike in 2022.

If the Bank forgoes a November rate rise the Pound could initially fall, but losses might prove shallow if the Bank offers guidance to suggest a December hike is likely - provided the November labour market report is strong.

Such guidance "could reduce the risk of some disappointment regarding the GBP," says Mialich.

But foreign exchange analysts at Goldman Sachs have told clients they are 'bearish' on the Pound's prospects in the near-term as the Bank of England will disappoint.

"The 'rubber meets the road' for the Bank of England, and markets have set a high bar for the MPC to deliver, essentially fully pricing a 15bp hike for this meeting and close to 60bp cumulatively through February," says Zach Pandl, an economist with Goldman Sachs.

The Wall Street bank says it will prove difficult for the Bank of England to significantly over-deliver at this point, and sets up room for disappointment if the MPC guides towards a more "measured" pace.

Such a "measured pace" would be a 15bp hike in November, followed by 25bp in February, which is Goldman Sachs' current expectation.

"This means that the risks are skewed towards GBP downside over the near term," says Pandl.