- Technicals favour AUD over GBP

- Short-term bounce in GBP/AUD becoming increasingly likely

- Strong market recovery favours AUD over G10 rivals

- Goldman Sachs back AUD from strategic perspective

Image © Adobe Images

![]() - GBP/AUD spot at time of writing: 1.8802

- GBP/AUD spot at time of writing: 1.8802

- Bank transfer rates (indicative range): 1.8150-1.8280

- FX specialist rates (indicative range): 1.8370-1.8640 >> more information

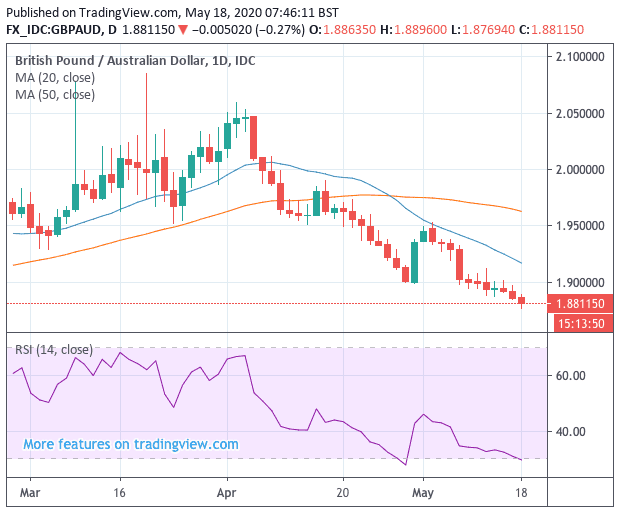

Pound Sterling remains entrenched in a multi-week sell-off against the Australian Dollar, leading us to retain a bearish stance on the GBP/AUD exchange rate at the start of the week.

Based on a number of key technical studies, the outlook near-term outlook is negative and Sterling is liable to further losses.

The exchange rate is 1.8808 at the time of writing and therefore below its 20 day moving average at 1.9170 and below its 50 day moving average at 1.9628. We would look for a move back above both MA's as an initial signal that the downtrend in GBP/AUD has come to an end, from where predictions for a more sustained rally in Sterling could be initiated.

Furthermore, the Relative Strength Index (RSI) is at 29 which suggests momentum remains in favour of further declines, as can be seen in the bottom pane of the graph below:

However, a reading below 30 also suggests the sell-off has technically reached oversold levels, from where a rebound could be expected. As can also be noted in the above graph, the RIS rarely spends time either below 30 or above 70.

The last time the RSI dipped below 30 was on April 29, the Pound-to-Australian Dollar bounced from a low of 1.8995 on April 29 to record a high of 1.9534 on May 04.

The bounce was short-lived and we would expect any rebounds from oversold conditions in GBP/AUD over the course of the coming week to similarly prove to be fleeting in duration and strength.

The fundamental financial and economic backdrop meanwhile remains supportive of the Australian Dollar, a currency that is expected to outperform its peers when stock markets and commodity prices are rising,

Asian and European markets start the week on a solid footing amidst ongoing confidence that the worst of the coronacrisis has now passed, with investors looking to the a recovery now that the world's economies are opening up once more. "Markets have started the week on a positive footing, but this is merely within the ranges of the last week or so. However, while equity futures are positive, the broader USD is mixed, with commodity currencies faring better as base and precious metals, along with oil prices extend recent gains," says Robin Wilkin, Global Cross Asset Strategist at Lloyds Bank.

The sentiment is most clearly expressed in the value of oil, which continues to recover rapidly on a combination of improving demand and restricted supply as the crisis ends the lives of many marginal producers.

The global recovery story is being lead by China which was the first country to lock down owing to the crisis, and was the first to open up again. This is proving beneficial for the Australian Dollar as China is Australia's largest export market, accounting for the lion's share of demand for iron ore, coal, natural gas and other raw materials of which Australia has an abundance.

Chinese demand for Australian exports is likely to step up as the government looks to boost spending on infrastructure projects as a way of stimulating the economy out of its coronavirus-inspired slowdown.

As long as the current market backdrop persists we would expect the Aussie Dollar to be bid higher. However, we warn that any secondary spike in covid-19 cases in any of the world's major economies could spark renewed anxiety which could in turn trigger bouts of 'risk off' market action, which would invariably negatively impact the Australian Dollar.

Foreign exchange strategists at Goldman Sachs - the Wall Street investment bank - meanwhile say they maintain a preference for the Australian Dollar from a strategic perspective, particularly against its New Zealand counterpart.

"One of the main rationales for this trade has been our view on relative monetary policy. The RBNZ appears much closer to further easing (including rate cuts into negative territory) than the RBA, and we see room for more to be priced, given the front-end implies just one 25bp cut to 0% over the next year, even after the RBNZ’s clearly dovish meeting last week," says Zach Pandl, co-head of global foreign exchange and emerging market strategy at Goldman Sachs in New York.

Goldman Sachs also still see a more favorable growth outlook for Australia than New Zealand, and Australia’s greater exposure to China demand (and commodity prices more broadly) should benefit Aussie more than Kiwi as China’s industrial activity continues to recover.

"That said, tensions have risen between Australia and China in recent weeks, and we think further escalation is a downside risk to AUD longs," says Pandl.

Domestic sentiment towards the Aussie currency deteriorated somewhat last week on news that China has suspended meat imports from four Australian companies that make up 35% of the country’s beef exports to China.

Beef is Australia's 8th largest export, accounting for 2% of the countries total export basket, according to Australia's Department for Foreign Affairs and Trade.

The move by China to ban what is effectively in the region of 35% of beef imports from Australia represents an escalation in tensions between the two countries after Australia called for a probe into the origins of the covid-19 pandemic.

It comes after China's ambassador to Australia said in a newspaper interview on April 27 that the Australian government's pursuit of an independent international inquiry into the coronavirus outbreak could spark a Chinese consumer boycott of students and tourists visiting the country, as well as sales of major exports including beef and wine.

"The beef import ban and the potential tariff on barley so far covers only a small share of Australia’s GDP," says Pandl.

China can do significant damage to Australia's exports, and therefore economy, if it so wishes and we would therefore imagine that the Australian government's tone on China's early handling of the coronavirus outbreak will ultimately remain measured. As such, this remains a small risk on the horizon for AUD.