Friday AM: GBP Finds Support, EUR at Risk of Further Losses, USD Eyes Third-quarter GDP

© IRStone, Adobe Stock

- USD could receive another boost from Friday GDP figures.

- GBP finds support at trendline near its September lows.

- EUR erodes support and is vulnerable to further losses.

The Pound, Euro and Dollar were unchanged early in the final session of the week, in a moment of inertia, following an overnight session that saw more weakness in global stock markets and ahead of the latest U.S. GDP data.

Stock markets, long seen as a gauge of investor confidence, are providing important signals to currency markets about investors' outlooks for the global economy and appetites for risk.

Currency market moves often influence stock prices but stock market moves rarely impact directly on currency markets.

However, the Dollar has drawn much of its 2018 strength from President Donald Trump's economic policies, which have enabled the Federal Reserve to raise interest rates while other central banks sit on their hands, and the U.S. stock market is a bellwether for the economy.

Moreover, U.S. corporate earnings updates are providing a steady drip of information about the likely economic impact of President Trump's trade war with China. As a result, moves in the U.S. Dollar have become more readily influenced by those of the American stock market in 2018 and the latter took another southward turn late in the Thursday session.

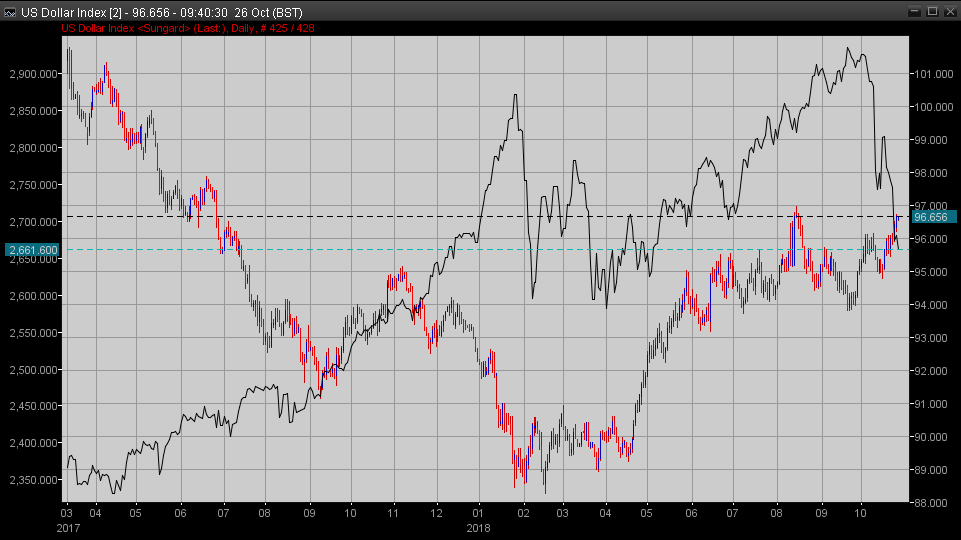

Above: U.S. Dollar index (red and blue) with S&P 500 (black) overlaid.

"Large intra-day moves in equities continue to drive FX. US stocks rallied hard into the close (S&P +1.8%) only to give up much of rise overnight on disappointing tech earnings announcements (NASDAQ future -1.5%). Directionally, risk proxies in FX slavishly followed, though moves are historically small in some pairs (see JPY below). Stocks are down almost 8% month-to-date which is likely to result in significant hedge-related USD buying when month-end comes into view next week," says Adam Cole, chief currency strategist at RBC Capital Markets.

Generally, weakness in the stock market has stemmed the rise of the Dollar but not weakened it, leading to inertia in currency markets. That rising correlation between stocks and the Dollar did exactly the same thing overnight, enabling the Pound-to-Dollar and Euro-to-Dollar rates to stabilise for a moment.

However, and regardless of whatever happens with the latest U.S. GDP figure due at 13:30 London time Friday, that stability is unlikely to last for long.

Advertisement

Bank-beating exchange rates! Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here

USD, Global Markets, Eye Third-quarter GDP

Consensus is for the U.S. economy to have expanded at an annualised pace of 3.3% during the third-quarter, down from a multi-year high of 4.2% previously.

However, data released on Thursday means there is a risk that this number is now too optimistic, according to some economists, although not everybody agrees.

"Our economists look for real GDP to print a 4-handle for the second straight quarter. Driving the advance is likely to be a considerable contribution from the consumer. Following robust core retail sales activity, expect real consumer spending to clock in at better than 3% q/q saar. Trade is expected to be a drag as exports are poised to slow sharply from their heady 9% clip in 2Q. This is all consistent with a 2018 full-year growth profile of about 3%," says RBC's Cole.

The U.S. economy is on track to grow by around 3% for 2018 overall, up from the 2.2% growth seen back in 2017, while others elsewhere in the world have either slowed already, or are seen decelerating in the months ahead.

That superior economic performance, brought about by President Donald Trump's tax cuts, enabled the Federal Reserve to keep raising interest rates at a time when other central banks have either dithered or sat on their hands.

The Fed has raised interest rates eight times since the end of 2015, and on three occasions in 2018, taking the Federal Funds rate range to between 2% and 2.25%.

This kind of aggressive monetary policy has seen the U.S. Dollar index convert what was once a 4% first quarter loss, into a 4.29% 2018 gain during the six months or so since the middle of April.

That outperformance from the Dollar has kept all other currencies on the back foot of late so markets will watch Friday's GDP figures closely for signs of a possible change in trend being on the horizon.

The U.S. Dollar index was quoted 0.09% lower at 96.58 during early trading Friday, close to its highest level since July 2017, while the USD/JPY rate was down 0.36% at 111.94.

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here

GBP Finds Support at September Low

With the U.S. Dollar frozen in the proverbial headlights overnight, the Pound-to-Dollar rate has stabilised at the tail-end of a 10 day period of losses but, once an initial correction higher has concluded, the exchange rate will be vulnerable to another downward leg according to one analyst.

"GBP/USD has sold off to the 78.6% retracement at 1.2798/85 and the 6 th September low, here we also find the 2016-2018 support line and we would allow for this to hold the initial test. This is seen as the last defence for the 1.2662 August low. Currently we would allow for a very small bounce towards 1.2950 ahead of further weakness," says Karen Jones, head of technical analysis at Commerzbank.

The Pound has fallen 1.8% against the Dollar in the last week and 2.7% during the October month, taking its 2018 loss over the 5% threshold.

Much of this decline has been due to the rampant strength of the Dollar but a substantial portion of it has also been driven by another roadblock having been reached in the Brexit negotiations.

Prime Minister Theresa May has so-far survived the uproar caused at home by her handling of the Brexit talks but with an agreement on terms of the U.K.'s withdrawal from the European Union not yet in the bag, and the March 2019 Brexit day drawing ever closer, political noise and pressure on the Pound has risen throughout October.

Disagreement over the so called "backstop" solution for managing the Northern Irish border in the event a deal on the future relationship cannot be struck at a later date has once again stymied progress.

Failure has led markets to begin contemplating the seemingly-increased risk of an exit from the EU without any kind of agreement whatsoever, which would see the U.K. default to trading with the bloc on World Trade Organization terms. Most economists say this would deal a blow to the U.K. economy.

The Pound-to-Dollar rate was quoted 0.05% lower at 1.2815 during early trading Friday, close to its September lows, while the Pound-to-Euro rate was 0.03% lower at 1.1268.

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here

Euro Erodes Support and is Eyeing another Leg Down

With the U.S. Dollar frozen in the proverbial headlights overnight, the Euro-to-Dollar rate has stabilised at the tail-end of its own multi-week period of losses.

However, the exchange rate is set for further declines and may need to fall as far as its August lows before traders can be convinced to prop it up with a renewed bid for the single currency.

"EUR/USD remains under pressure following its recent failure at the 20 day ma at 1.1499 and has eroded support at 1.1411/15, the 78.6% retracement and 2017-2018 support line. At this point we will assume that there is scope for a retest of the 1.1319 200 week ma and 1.1301 recent low. This is expected to hold the down side. We will attempt to buy this dip," says Commerzbank's Jones.

The Euro has suffered steep losses against the Dollar this month thanks to a continued advance by the greenback as well as a combination of headwinds having conspired to haunt the single currency. It has declined -1.14% this week and 3.1% in the last month, taking its 2018 loss to 5.1%.

A destabilising row between the Italian government and European Commission, over the former's budget policies, risks stoking anti-Euro and anti-EU sentiment in the Mediterranean country. That, and the government's policies, now threaten the nation's place within the Eurozone currency bloc.

Italy's row with Brussels has taken place as investors the world over grapple with the possible adverse implications of President Trump's so called trade war against China, and as the economic outlook for the single currency bloc has darkened. A series of indicators of Eurozone growth have turned lower in recent months, leading markets to fear for the inflation and European Central Bank (ECB) policy outlook.

For its part, the ECB said Thursday it will not be deterred from ending its quantitative easing programme at year-end, or from normalising its interest rate structure once into 2019, by recent developments. But the central bank could easily be forced into doing so if the economic environment deteriorates to such an extent that it undermines the already-fragile outlook for consumer prices.

The ECB's policy pledges are what has prevented the Euro from handing all of 2017's double-digit gain back to a resurgent U.S. Dollar this year, but those commitments are contingent on an economic performance that supports a sustained return of inflation toward the central bank's target of "close to but below 2%".

Eurozone inflation rose by 2.1% during September however, core inflation posted a surprise 20 basis point fall to 0.9%. The core measure removes volatile commodity items from the goods basket so is thought to provide a better reflection of domestically generated price pressures. With this rate still being firmly subdued, the ECB could find it increasingly difficult to justify normalising its monetary policies, particularly if the economic outlook deteriorates further in the months ahead.

The Euro-to-Dollar rate was quoted 0.01% higher at 1.1376 Friday while the Euro-to-Pound rate was 0.02% higher at 0.8873.

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here